What is the Techno-Dollar? The idea that just as Saudi oil created sustained global dollar demand in the 1970s — American AI may be doing something similar today. The AI stack is heavily dollar-denominated at the infrastructure layer — from chips to cloud to frontier model access. As the world buys AI infrastructure, it often buys into the dollar system too.

Does AI actually strengthen the dollar? Short answer: yes, structurally — with a major caveat below. AI demand creates real, sustained dollar demand, but the dollar still had its worst H1 in 50 years during 2025, the same window NVIDIA’s revenue was setting records. AI appears to be a partial structural support, not a force strong enough to override bigger cyclical pressures on its own. DeepSeek cracked the first wall. EU regulations are building the second. And China is constructing an entire AI ecosystem outside the dollar.

Is this the new petrodollar? Similar demand-creation mechanism. Different capital flow underneath. Same question: how long does it last?

Core Thesis The Petrodollar era was built on global demand for oil. The Techno-Dollar era may be built on global demand for AI compute and cloud infrastructure. As long as the world’s most important AI infrastructure remains American and dollar-denominated, every AI boom becomes a dollar-demand event.

Prologue: A Room in Riyadh, and a Server Farm in Virginia

1973. The world was reeling from the oil crisis.

In the years that followed, the United States and Saudi Arabia developed a strategic relationship that encouraged oil trade to remain heavily dollar-denominated. Over time, Saudi surplus dollars were increasingly recycled into US financial markets — Treasury bonds, American assets, Wall Street instruments — helping reinforce what would become known as the petrodollar system.

No single treaty. No signed agreement made public. Just the architecture of mutual interest between powerful nations — and a currency that happened to be at the centre of it all.

2026. No room. No handshake. No deal.

Just a server farm in Virginia, a data centre in Singapore, a GPU cluster in Tokyo — all running on chips that cost $30,000 each, all denominated in one currency.

Dollars.

The structural logic is similar. The fuel has changed. Oil has been replaced by something faster, lighter, and potentially more addictive.

Intelligence.

Chapter 1: 1973 and 2025 — Two Loops, One Currency

To understand the Techno-Dollar, you first need to understand why the Petrodollar worked so well.

The world didn’t run on oil because someone decided it should. The world ran on oil because oil was the most efficient energy source available — and Saudi Arabia controlled some of the world’s largest and cheapest oil reserves. The 1973 oil embargo exposed how much leverage that gave them. By 1974-75, that leverage had been formalized: Saudi oil, priced in dollars.

The loop was simple and brutal:

Japan needs oil → Japan buys dollars → Japan buys Saudi oil in dollars → Saudi Arabia has surplus dollars → Saudi Arabia buys US Treasury bonds → America can borrow cheaply → America buys more things from Japan.

The loop created persistent demand for dollars. None of them chose this directly. It was the architecture of necessity.

Now look at today.

A startup in Bangalore wants to build an AI product. They need compute. They go to AWS, Google Cloud, or Microsoft Azure — global enterprise contracts are usually dollar-denominated at the infrastructure layer. Their NVIDIA H100 GPUs cost roughly $30,000 each — priced in dollars. Their OpenAI API calls are billed in dollars. Many of their AI engineers are paid through platforms that settle in dollars.

A hospital in Germany wants to run AI diagnostics. Microsoft Azure. Dollars.

A bank in Brazil wants AI-powered fraud detection. Google Cloud. Dollars.

A factory in Vietnam wants AI-driven supply chain optimization. AWS. Dollars.

The loop has quietly rebuilt itself. Similar demand-creation mechanism. Different commodity. Same currency. As later chapters will show, the capital-recycling mechanism underneath it is not the same — and that difference matters more than it first appears.

Chapter 2: NVIDIA Dollar Demand and the $200 Billion Milestone

To put that in perspective: NVIDIA’s FY2026 revenue alone was larger than the entire GDP of countries like Finland, Portugal, or New Zealand.

And the most recent quarter — Q1 of fiscal year 2027, ended April 26, 2026 — NVIDIA reported $81.6 billion in a single quarter, per its official earnings release. In three months. More than most Fortune 500 companies make in a year.

The infrastructure layer behind it is overwhelmingly dollar-denominated.

NVIDIA’s global enterprise pricing is set almost entirely in dollars. When Japan’s SoftBank builds out its AI computing platform — over 10,000 NVIDIA GPUs across Ampere, Hopper, and Blackwell generations by mid-2025, including the world’s largest operating DGX SuperPOD deployment — it pays in dollars. When Saudi Arabia’s NEOM project deploys AI infrastructure, when India’s Reliance builds out its AI data centres — both transact in dollars too.

And even where local billing arrangements exist — a European company paying Azure Europe in euros, for instance — the dollar demand doesn’t disappear. It just moves one step back in the chain.

Imagine a designer in Nairobi paying a coder in Hanoi for some freelance AI fine-tuning work. Neither one wants dollars. Neither one is thinking about American monetary policy. They just want to get paid, and get paid promptly.

Yet the payment still touches dollars.

Why?

Because the global financial system speaks one common language — and it isn’t shillings or dong.

A direct shilling-to-dong market barely exists. Too little liquidity, too few traders, too much risk for any bank to hold inventory in both currencies. So the payment gets routed through an intermediary currency that every bank in the world holds reserves in and trusts completely.

Shilling → Dollar → Dong. The dollar is the bridge — not because either party wants it, but because the global financial plumbing has no other pipe to run the transaction through.

Economists call this the dollar’s role as a “vehicle currency.” According to the Bank for International Settlements’ 2025 Triennial Survey, the dollar was on one side of 89% of all global foreign exchange trades — not because everyone needs dollars specifically, but because it’s the only currency liquid and trusted enough to act as the universal middleman between everything else.

This is why Azure Europe’s euro billing doesn’t actually escape the dollar system. Microsoft’s global treasury operations, its capital markets activity, the chips it buys from NVIDIA, the cross-border settlement of its own revenues — much of it eventually touches dollar-denominated infrastructure, even when the customer-facing invoice says €.

The dollar demand is structural, not just transactional. It doesn’t require every payment to be in dollars. It only requires the global financial system to keep needing a common bridge currency — and right now, nothing else comes close.

Now, an honest pause.

This vehicle-currency mechanism isn’t unique to AI. The same shilling-to-dollar-to-dong routing would happen whether that Nairobi-Hanoi payment was for AI fine-tuning work, a shipment of furniture, or a consulting invoice. The dollar’s 89% share of FX trades reflects its role across all global trade. AI doesn’t bend that mechanism. It just rides it.

So what makes AI worth a separate story at all? Not a different mechanism. Scale, and how fast that scale is growing. Global AI spending is on a trajectory toward $1.2-2.5 trillion within a few years — a genuinely large, genuinely new addition to the volume moving through the dollar’s vehicle-currency role. That’s a more modest claim than “AI is structurally different from other trade.” But it’s the one the evidence actually supports.

And here’s the thing people miss when they talk about NVIDIA.

NVIDIA is not important because it sells chips. NVIDIA is important because it sells access to intelligence.

In the 20th century, countries competed for oil fields. Whoever controlled the oil field controlled the energy supply. Whoever controlled the energy supply had leverage over everyone who needed energy.

In the 21st century, the fight may be over compute clusters instead. Whoever controls frontier compute may influence access to advanced machine intelligence. Whoever influences that access holds leverage over everyone who needs it.

Right now, NVIDIA controls the compute cluster’s design and pricing. America currently dominates the most valuable layers of the compute stack.

But a fair question lands here, and it deserves a real answer, not a dodge.

Boeing sells aircraft globally, priced in dollars. Apple sells iPhones globally, priced largely in dollars. Microsoft, Adobe, Netflix — all American, all dollar-denominated, all generating real dollar demand. Nobody calls any of them a “Boeing-Dollar” or an “iPhone-Dollar.” So why does AI get a special name?

The honest answer: AI isn’t different because it’s American. It’s potentially different because of what it might become.

An iPhone is a finished product — you buy it, you use it, you replace it in a few years. Boeing builds aircraft, a capital good with a long, predictable replacement cycle. Both are real industries. Neither is something every other industry needs just to function.

There’s a sharper version of this same objection, and it’s worth sitting with too: why AI, and not just cloud computing? AWS existed years before ChatGPT. Azure existed before GPT-4. Couldn’t this whole thesis just be an old cloud-computing story wearing a new label?

The distinction is real, even if it’s easy to miss at first glance. Cloud computing sells computing capacity — storage, processing power, the raw ability to run any kind of software at scale. It doesn’t care what you do with it. AI sells something narrower, and potentially far more consequential: decision-making capacity. Not just the ability to run software, but the ability to draft a contract, read an X-ray, write code, negotiate a price, reroute a shipment in real time. If AI gets woven into every white-collar workflow the way cloud computing got woven into every IT department, its economic role starts looking less like infrastructure and more like labour — and labour has never been priced as cheaply, or commoditised as quickly, as raw compute. That’s the real basis for calling this something distinct from “Cloud-Dollar,” not just a rebrand.

Oil earned its place in the global economy not because it was American-adjacent, but because every other industry depended on it to run — factories, transport, agriculture, manufacturing, all of it. The Petrodollar was never about oil being a good product. It was about oil being unavoidable.

AI’s claim to a similar role rests on one bet: that it becomes a universal production input too — not just something people buy, but infrastructure every knowledge-based industry eventually runs on, the way electricity or the internet did before it. If that bet is wrong — if AI stays a category of software people buy, more like Adobe than like oil — then “Techno-Dollar” collapses into something far less interesting: “America has profitable export industries.” True, but not new, and not worth a special name. Right now, the trajectory points toward infrastructure. But it’s still a bet, not a settled fact.

And even if that bet pays off, there’s a deeper paradox waiting on the other side of it.

Nobody buys dollars because they use electricity. Nobody buys dollars because a website loads over TCP/IP. Infrastructure, once it fully succeeds, tends to vanish into the background — it gets cheap, commoditised, locally embedded, until the original supplier simply stops mattering.

There’s a real, checkable case for exactly this pattern. Arguably the most universal production input in modern history: electricity. American companies — Edison, Westinghouse, General Electric — pioneered much of the technology that lit up the world. There is no “Electro-Dollar.” There never was. Electricity generation got localized, nationalized, regionalized almost everywhere, precisely because once the technology matured, every country built its own grid instead of leaning on American supply forever. The thing became too important to leave in one country’s hands.

Worth a small caveat on how far this analogy actually travels: electricity localized partly for a physical reason — you lose power over long transmission distances, so building generation close to where it’s consumed is simply more efficient. AI’s path to localizing, if it happens, would be different in kind — driven by economic forces like model compression and distillation shrinking what once needed a data centre down to something that runs on a laptop, not by anything as physically unavoidable as transmission loss. The analogy illustrates the pattern well. It shouldn’t be read as proof the timeline will match.

If AI follows that same arc — if compute gets cheap enough to run locally, on a phone or a laptop, instead of through a metered call to an American data centre — this whole compute-dollar loop could start fading at the exact moment AI is everywhere, the same way electricity’s importance kept climbing long after America’s grip on it had already slipped away. The real bet underneath this whole article isn’t just “AI becomes infrastructure.” It’s “AI becomes infrastructure while staying scarce and centrally supplied.” That’s a narrower, more fragile bet than “AI becomes important” alone — and electricity’s own history suggests bets like that rarely hold for long.

The math, for now: global AI demand currently translates disproportionately into NVIDIA demand, and therefore disproportionately into dollar demand. Whether that holds as DeepSeek, Mistral, Qwen, and Huawei’s stack mature is the question the rest of this article keeps coming back to.

But NVIDIA is just one company. The full picture is bigger.

The Global AI Market:

2025: ~$300-400 billion (estimates vary by methodology)

2030 projection: $1.2-2.5 trillion (Grand View Research, Fortune Business Insights)

North America’s share: ~35% of global AI market — but American companies dominate the infrastructure layer globally

The infrastructure layer is the key phrase. You can build AI applications in any language, any country. But the chips, the cloud compute, the foundation models — these are overwhelmingly American. And overwhelmingly dollar-denominated.

There’s a name missing from this story so far. And it matters more than NVIDIA’s.

NVIDIA designs chips. It does not make them.

Every H100, every Blackwell, every chip carrying NVIDIA’s logo is physically built by one company, in one country: Taiwan Semiconductor Manufacturing Company — TSMC. As of 2025, TSMC manufactures roughly 90% of the world’s most advanced logic chips — effectively all of NVIDIA’s leading-edge silicon passes through its fabs before it touches a data centre.

This isn’t a footnote. It’s the actual chokepoint underneath everything this article has described so far.

Strip away the $216 billion in FY2026 revenue, the design supremacy, the software moat built into CUDA — none of it produces a single working chip without two factories in Hsinchu and Tainan. America doesn’t manufacture frontier AI chips. Taiwan does. The Techno-Dollar thesis leans on American control of compute. But American control of compute leans, in turn, on Taiwanese control of manufacturing — sitting roughly 180 kilometres off the coast of a country that has openly stated its intent to reunify with it, by force if necessary.

So picture the stack as a building, not a single block. America owns the penthouse — the design and the revenue capture: NVIDIA’s architecture, CUDA’s lock-in, the dollar-denominated billing that flows from all of it. But walk down a few floors and the ownership changes. TSMC, fabricating the chips, is Taiwanese. ASML, building the extreme ultraviolet lithography machines without which none of this works, is Dutch. ARM, whose architecture sits under much of the world’s computing, is British. Rare earth processing — critical to chip manufacturing — is overwhelmingly Chinese. America’s dominance is real. It just isn’t load-bearing all the way down.

A serious disruption to TSMC specifically — geopolitical, military, or otherwise — would shake this entire AI-driven dollar demand loop harder than DeepSeek or the EU AI Act ever could. DeepSeek and EU regulation change the price of compute, or who supplies it. A disruption at TSMC would constrain the supply of compute itself, everywhere, all at once.

So the Techno-Dollar, stripped down, is American demand-side dominance sitting on top of a Taiwanese supply-side chokepoint. This article has spent most of its energy on the half that’s easy to measure in dollars. The half that’s easiest to disrupt with a blockade is the other one.

Keep that crack in the foundation in mind. Because the next chapter isn’t just about software getting cheap. It’s about what happens when software gets cheap and the hardware underneath it was never fully American to begin with.

Chapter 3: The Petrodollar Playbook — Rewritten in Silicon

In 1974, oil was the ultimate scarce resource. You couldn’t run a factory without it. Couldn’t heat a home without it. Couldn’t move a single container ship without it.

America didn’t produce the most oil. But America controlled the pricing layer — through the Saudi deal, through OPEC relationships, through dollar invoicing.

Today, compute is the new scarce resource.

You can’t train a frontier AI model without GPUs. You can’t run real-time inference at scale without cloud infrastructure. You can’t reach the best foundation models without API access.

America doesn’t manufacture everything. But America dominates the pricing layer — through NVIDIA’s chip design leadership, through AWS, Azure, and Google Cloud’s grip on the market, through OpenAI, Anthropic, and Google’s lead on the models themselves. “Dominates,” not “controls” — Huawei, Alibaba Cloud, and DeepSeek already exist, and they’re growing. The dominance is real. It isn’t exclusive.

The parallels aren’t coincidental. They’re structural.

Petrodollar (1974-75)

Techno-Dollar (2025)

Scarce resource

Oil

AI Compute

Dominant supplier

Saudi Arabia

NVIDIA / US Cloud

Currency of transaction

US Dollar

US Dollar

Who sets the price

OPEC (US-aligned)

American tech companies

Who needs it

Every industrial economy

Every digital economy

Dollar demand created

Massive, sustained

Growing rapidly, but structurally different

But there’s a scale mismatch most arguments for this AI-dollar dominance thesis quietly skip past. And it matters.

The global oil market trades roughly $2-3 trillion every single year. Oil is a recurring, non-durable cost — you burn it, it’s gone, you buy more next month. Forever. That’s what made the Petrodollar loop self-sustaining for fifty years. It never needed a second sales pitch.

AI compute, right now, is overwhelmingly CapEx, not OpEx. Companies are buying chips once. A $100 million GPU order doesn’t automatically repeat next year. Microsoft, Google, and Meta are mid-way through an infrastructure land grab — not settled into a recurring consumption cycle. NVIDIA’s extraordinary growth right now partly reflects exactly this: everyone building out their AI capacity at the same time, in the same window.

So the real question for this compute dollar loop’s longevity isn’t whether the land grab continues. It’s whether it ever converts into recurring revenue.

If the world shifts from buying chips once to paying monthly API fees and per-token charges forever — inference costs, not training costs — the Techno-Dollar starts to look like oil: a permanent, repeating event. If AI infrastructure spending simply plateaus once the current buildout finishes, the whole comparison weakens considerably.

This is where AI agents change the equation.

A trained model is a one-time purchase. An AI agent running continuously — answering customer queries, processing transactions, writing code, watching infrastructure, all day, every day, with no off switch — is a different animal. Every workflow it runs is an inference event. Every inference event burns tokens. And right now, almost every one of those tokens is billed through a dollar-denominated platform.

If AI shifts from “train once, deploy once” to “agents running billions of times a day, forever,” that’s the moment the Techno-Dollar stops looking like a one-time purchase and starts looking like fuel consumption. Burned, gone, bought again tomorrow. Exactly like oil.

The CapEx wave is real, and it’s happening right now. Whether it becomes an OpEx river — fed by trillions of agentic inference calls instead of one-time training runs — is the open question that decides whether the Techno-Dollar lasts five years or fifty. And it’s worth being honest: nobody knows yet whether enterprises will actually deploy agents at that scale. This is a forecast about where AI economics might go, not a description of where they already are.

Now for the uncomfortable test. Does any of this actually show up in the dollar itself?

If this AI-driven dollar demand thesis holds, you’d expect NVIDIA’s extraordinary 2025-2026 revenue growth to line up with a strengthening dollar.

It didn’t.

In the first half of 2025 — the same window NVIDIA’s revenue was accelerating toward its FY2026 record — the DXY, the dollar index that tracks the dollar against a basket of major currencies, fell roughly 10-11%. Worst H1 performance for the dollar in over fifty years. It lost ground against almost everything — down double digits against the euro and the Swiss franc, down against the yen too. Morgan Stanley called it the end of a fifteen-year structural bull run that had lasted from 2010 to 2024. By the close of 2025, the dollar had fallen close to 10% for the full year.

Record AI-driven dollar demand. The worst dollar selloff in half a century. Happening at exactly the same time.

This doesn’t kill the underlying thesis. But it does mean the thesis needs a more careful claim than “AI demand makes the dollar strong.”

Here’s the more honest version: two different forces were pulling on the dollar at once, at different speeds, for different reasons.

The cyclical forces — the ones actually moving the DXY through 2025 — were Federal Reserve rate cuts, new tariff policy under the Trump administration, growing worry about the $39 trillion federal debt, and the unwinding of a dollar rally that had run for over a decade. Think of these like weather. They shift fast, and they can reverse with the next rate decision or the next election.

The structural force this article has been tracing — AI infrastructure spending creating sustained, multi-decade demand for dollar-denominated chips, cloud, and compute — moves more like climate. Slower. Underneath the weather, not instead of it.

So don’t think of it as “AI demand keeps the dollar strong.” Think of it as: AI demand is one of the few genuinely new sources of dollar demand showing up at a moment when several older sources — oil pricing, automatic reserve-currency status, predictable US fiscal policy — are each weakening at the same time. The Techno-Dollar probably isn’t powerful enough to override a determined cyclical selloff on its own. What it might do is set a floor under the dollar’s long-term decline that wouldn’t otherwise be there.

That’s a smaller, more defensible claim than “AI makes the dollar dominant.” It’s also more interesting, because it changes what the real test looks like. The test isn’t whether the dollar goes up. It’s whether the dollar’s decline, the next time cyclical pressure returns, is shallower and slower than it would have been without a trillion-dollar AI infrastructure boom sitting underneath it.

We won’t know the answer for years. But an article that quietly skips this tension isn’t being rigorous. This one shouldn’t.

The difference between oil and AI is real. It’s just not where most people look for it.

Oil is a physical commodity. It can run out. Get replaced. Get discovered somewhere new.

AI has two layers, and they behave in opposite ways.

The hardware layer — the chips, the fabs, the physical compute — behaves like oil. Capital-intensive, slow to build, genuinely scarce. NVIDIA’s moat here is real: TSMC’s fabrication capacity, the engineering talent, years of R&D baked into every new generation of chips. This layer actually deepens with use, because more revenue funds more R&D, which widens the technical gap even further.

The software layer — the models, the weights, the techniques — behaves nothing like oil. It behaves like water. It copies. It leaks. The moment someone reverse-engineers the approach, it spreads.

DeepSeek is the most dramatic example of this, but it’s far from the only one. France’s Mistral AI competes credibly with American models on a fraction of the funding. Alibaba’s Qwen and Meta’s open-weight Llama get downloaded and fine-tuned by developers everywhere, no permission required. Google has open-sourced parts of its Gemini research. Same pattern, repeated across multiple labs, multiple countries, multiple corporate incentives: once a capability gets demonstrated once, it tends to get replicated, compressed, and commoditised within months, not years.

The entire Techno-Dollar thesis rests on one bet: that the hardware moat stays scarce even as the software moat erodes underneath it.

So far, it has. NVIDIA still controls the physical chips. But DeepSeek’s R1 and V4 releases showed, more visibly than any single competitor had before, that you don’t need the most expensive chips if your software is efficient enough. And the fact that Mistral, Qwen, and Llama show similar — if less dramatic — efficiency gains suggests this isn’t a one-company fluke. It’s a structural feature of how software competition works. The software layer’s erosion can partially neutralise the hardware layer’s scarcity, no matter which lab happens to demonstrate it first.

If oil was a river of dollar demand, AI’s hardware layer could be an ocean. Its software layer is already a leak in the dam.

The difference comes down to this: oil created dollar demand through energy dependence. AI creates it through compute dependence. One powered factories. The other may end up powering intelligence itself.

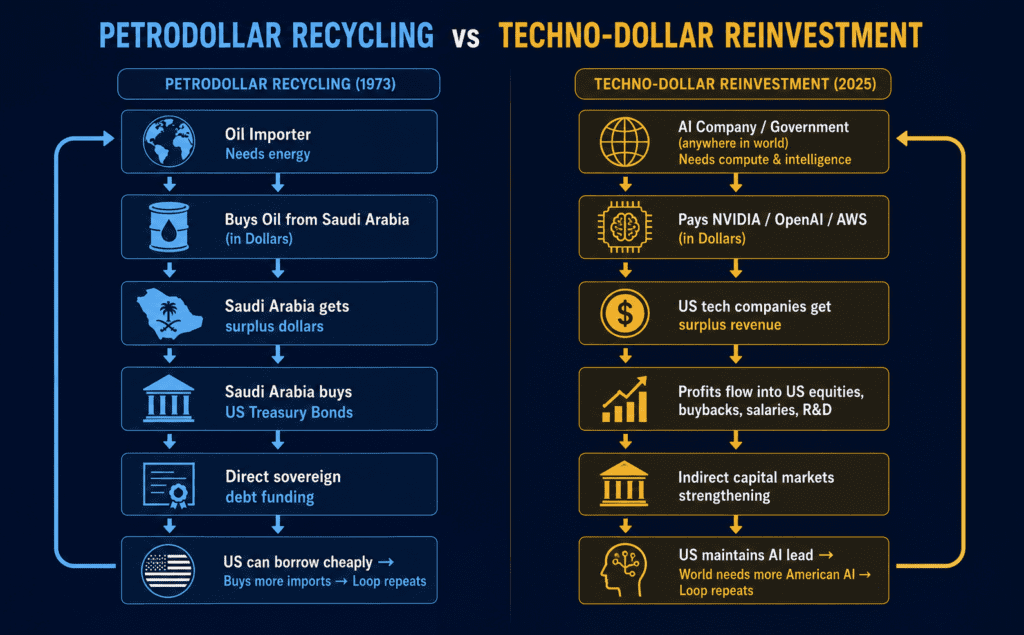

[INFOGRAPHIC — “Petrodollar Recycling vs Techno-Dollar Reinvestment”]

One honest distinction worth flagging here, even briefly.

The Petrodollar wasn’t powerful just because oil was priced in dollars. It was powerful because of what happened next — Saudi surplus dollars flowed straight into US Treasury bonds, funding Washington’s debt for decades. NVIDIA and Microsoft’s surplus dollars don’t do that. They fund buybacks and R&D instead. Call it reinvestment, not recycling — a distinction big enough that this article comes back to it in full later, in a section called The Treasury Test.

Key takeaway

AI creates structural dollar demand, but doesn’t fund US debt the way oil money did.

Chapter 4: The DeepSeek Moment — When the Wall Cracked

January 20, 2025.

A Monday morning. Silicon Valley was still celebrating its own dominance.

Then a Chinese lab called DeepSeek dropped a model called R1.

It matched OpenAI’s best reasoning models on most benchmarks.

Training cost? Here’s where it gets interesting — because the real number depends on which layer you’re measuring, and on what people actually knew at the time.

Back in December 2024, DeepSeek had published a paper disclosing the cost of its underlying base model — DeepSeek-V3, the foundation R1 was built on top of. Estimated at $5.6 million to train, based on disclosed GPU-hour figures: 2,048 H800 chips, roughly 55 days. That figure, plus DeepSeek’s broader efficiency claims, is what the market was actually reacting to on January 20th.

The number everyone remembers now — $294,000 — is something else entirely. It’s the cost of just R1’s reasoning layer, the reinforcement-learning stage that turned V3 into a model that could think step by step. 512 H800 chips. 80 hours. But it wasn’t disclosed until much later, in a peer-reviewed Nature paper published in September 2025 — eight months after the crash. Nobody trading NVIDIA stock that January knew this number existed. It only entered the story in hindsight.

Add both together, and the realistic estimate lands around $5.9 million — built from disclosed and inferred figures, not an audited number — and even that excludes prior research, failed experiments, and the actual hardware purchase cost, which industry estimates put well above $50 million once you count the full GPU cluster.

OpenAI’s GPT-4? $600 million-plus.

Even using just the $5.6 million figure the market actually had in January — not the more dramatic $294,000 number that surfaced later — that’s still roughly one-hundredth of the price. For comparable performance.

The reaction was instant, and brutal. NVIDIA’s stock fell so hard in a single day that it wiped out $600 billion in market cap — the largest single-day loss in stock market history, for any company, ever.

$600 billion. Gone. In one day.

Because the market suddenly asked a question it had never seriously had to ask before:

“If China can build frontier AI at a hundredth of the cost — do you actually need NVIDIA’s chips? Do you actually need American cloud? Do you actually need to pay in dollars?”

The DeepSeek cost comparison, laid out plainly, is genuinely staggering:

Metric

OpenAI o1 / GPT-4

DeepSeek R1

API cost per million input tokens

$15

$0.55

API cost per million output tokens

$60

$2.19

Total training cost (base model + reasoning layer)

$600M+

~$5.9M

R1 reasoning layer alone (RL stage, on top of base model)

—

$294K

Performance gap

Baseline

Matches on math/coding benchmarks

Run the numbers on something concrete. Processing 100 million tokens costs roughly $1,500 on OpenAI. On DeepSeek? About $55.

That’s not an incremental improvement. That’s a 96% cost cut. A paradigm shift, not a discount.

And DeepSeek pulled it off using older NVIDIA chips — H800s, not the cutting-edge H100s America had specifically restricted China from buying. They optimized so hard they ended up needing less of exactly what America was trying to deny them.

The uncomfortable implication sits underneath all of it: if you can build comparable AI without the most expensive American chips, the entire Techno-Dollar loop has a soft spot. Dollar demand from AI compute was never guaranteed. It depends on American AI staying the only viable option.

DeepSeek showed it isn’t.

Chapter 5: China’s Parallel Universe — The Dollar-Free AI Stack

DeepSeek wasn’t an accident. It was a symptom.

China has been building a parallel AI universe for years now — deliberately, systematically, patiently — outside the dollar ecosystem entirely.

Here’s the architecture of that dollar-free stack, piece by piece.

The Huawei V4 Proof Point

Chips. America restricted NVIDIA H100 exports to China. China answered by accelerating Huawei’s Ascend chip program. The clearest proof point landed on April 24, 2026, when DeepSeek released its V4 model family — V4-Pro, a 1.6-trillion-parameter model, and V4-Flash — and handed Huawei and other Chinese chipmakers exclusive early optimization access, while deliberately shutting NVIDIA and AMD out. Huawei confirmed day-zero support across its Ascend 950 line.

Eight days before that release, NVIDIA CEO Jensen Huang had warned on the Dwarkesh Podcast that “DeepSeek coming out on Huawei first” would be “a horrible outcome” for the US. Then it happened.

Worth flagging up front, before going any further: even Huawei’s own chip supply chain isn’t fully sealed off from the dollar world. SMIC, the domestic Chinese foundry now handling most Ascend production, still depends on Dutch ASML lithography tools and other globally-sourced equipment to do it. (TSMC, notably, isn’t part of this picture — it’s been legally barred from supplying Huawei since September 2020, and Taiwan formally closed the loophole that let some chips slip through anyway by adding Huawei to its own export-control entity list in 2025.) Plenty of the raw materials involved in chip manufacturing are still priced or financed in dollars somewhere along the way, too. “Chinese chips” doesn’t yet mean “dollar-free chips,” not entirely. Keep that in mind as the rest of this stack comes into view.

What’s still genuinely contested is the training side of the V4 story. A senior US official alleged it was trained on smuggled NVIDIA Blackwell chips. DeepSeek denies it, says it used H800 and Huawei Ascend 910C chips instead. A Tsinghua professor told MIT Technology Review the model may still have been trained mainly on NVIDIA hardware regardless. NVIDIA itself published a same-day technical blog showing V4-Pro running at full speed on its own Blackwell chips. So here’s the part that’s actually verifiable: exclusive early access and inference deployment went to Huawei. Where the training itself happened is still disputed. Even with that asterisk, Huawei trails NVIDIA on raw technical capability, and pulling the broader developer ecosystem away from NVIDIA remains genuinely hard. But the direction of travel is no longer in question.

Cloud. Alibaba Cloud, Tencent Cloud, Huawei Cloud — all priced in yuan. A Chinese company building AI today can route most of its spending through this layer without touching a dollar directly.

Foundation models. Baidu’s ERNIE. Alibaba’s Qwen. ByteDance’s Doubao. DeepSeek itself. Increasingly competitive with American models — and priced in yuan.

Data. China has more internet users than the US and Europe combined. The training data pool is enormous, and it sits entirely in Chinese hands.

Put the four pieces together, and here’s what falls out: a Chinese startup building AI in 2025 can run on Chinese chips, Chinese cloud, Chinese foundation models, Chinese payment systems — and dramatically cut its exposure to dollar-based AI infrastructure.

“Never touch a dollar” would still be too strong a claim overall, and it’s worth restating plainly, not just as a footnote. Huawei’s own chip fabrication still leans, indirectly, on global semiconductor equipment supply chains that aren’t fully dollar-free, as just noted. Plenty of the raw commodities and specialized tools in chip manufacturing are still priced or financed in dollars somewhere upstream. And China’s own capital markets, whenever they touch the rest of the world, still run substantially through dollar-denominated channels. The exposure is reduced. Not erased.

Still — that’s new. As recently as 2020, even this reduced exposure wasn’t possible. Today it is.

And China is actively exporting this stack to the rest of the world.

Belt and Road countries — Pakistan, Indonesia, Ethiopia, Bangladesh — are receiving Chinese AI infrastructure investment right now. Chinese cloud. Chinese models. Chinese compute. All settled in yuan or local-currency arrangements.

If a country builds its AI infrastructure on Chinese stacks, its AI-related dollar demand falls dramatically — even if it doesn’t disappear entirely, for the same upstream supply-chain reasons just laid out.

The Techno-Dollar loop doesn’t just need American AI to be good. It needs American AI to be the only AI the world has access to.

That window is closing.

And here’s why America restricted those chips in the first place.

It wasn’t only about slowing China’s military. It was about something simpler, and more fundamental.

The United States restricted advanced AI chips because it understood one thing clearly: whoever controls the compute layer may shape the future economic layer. And whoever shapes the future economic layer may, in turn, influence the future monetary layer.

Chips → Intelligence → Economic power → Monetary influence.

That’s the chain — at least as a hypothesis. The export controls may have looked like national-security policy on the surface, but they carried monetary implications underneath. Control the compute layer, and you may end up influencing the monetary layer too.

China appears to understand the exact same chain. Which is why it’s building Huawei’s Ascend. Why DeepSeek optimized around the chips it was denied. Why Beijing is funding a domestic AI stack with an urgency that echoes how America once funded its own nuclear program.

Both sides are fighting over compute. Because both sides suspect what compute might eventually control.

Key takeaway

China has built a working alternative to American AI infrastructure — chips, cloud, models, and data — that’s reduced, not eliminated, its dollar dependency.

Chapter 6: The Regulatory Chokehold — Europe’s Quiet Rebellion

There’s a third force at work here — quieter than DeepSeek, slower than China, but potentially the most lasting of the three.

Regulation. And underneath it, a genuine sovereignty push that’s moved well past paper.

The EU AI Act, passed in 2024, is the world’s first comprehensive AI law. It classifies AI by risk level — high-risk uses in hiring, credit scoring, medical diagnosis, and critical infrastructure face strict transparency and oversight requirements. American companies sit directly inside that scope.

Italy showed the template early. In March 2023, Italy’s data protection authority banned ChatGPT for several weeks over GDPR concerns — the first Western democracy to block a major American AI tool. It came back a few weeks later. But the precedent stayed.

Regulation is only half the story, though. Europe’s sovereignty push is real — but the numbers say it’s still mostly aspirational. Roughly 90% of Europe’s digital infrastructure remained controlled by non-European, mostly American, firms as of late 2025, according to one competition economist’s estimate. The shift underway is directional, not present-tense. With that firmly in view, here’s what Europe has actually been building.

Take Gaia-X, Europe’s cloud sovereignty framework, launched back in 2020. For years it earned exactly the criticism you’d expect of a framework that sounds good in a press release and changes nothing on the ground — American hyperscalers were even allowed to join Gaia-X itself, which critics labelled a “Trojan horse” diluting the entire point. That criticism was fair, for a while. But by 2025-26, several hundred cloud services had actually passed Gaia-X certification, under a new tiered sovereignty system — Level 3, the highest tier, reserved specifically for EU-headquartered providers. German firms like SAP, Deutsche Telekom, and IONOS built sovereign cloud stacks designed to run without leaning on US hyperscaler infrastructure at all. Deutsche Telekom alone put over €1 billion behind a Munich-based “Industrial AI Cloud,” up to 10,000 GPUs, run exclusively by European staff.

Then in June 2026, the European Commission went further still — proposing a Cloud and AI Development Act, a sovereignty framework aiming to triple EU data-centre capacity within five to seven years.

None of this means Europe has actually decoupled, though, and it’s worth being honest about the gap. Even AWS’s own “European Sovereign Cloud,” launched in Brandenburg in January 2026 with a dedicated EU-based legal entity, is still ultimately owned by a US parent company — and still subject to the US CLOUD Act. A concession to sovereignty pressure, not sovereignty itself. Forrester predicted no European enterprise would fully exit US hyperscalers in 2026.

Still, the dollar implication is simple, even carrying that caveat.

If European companies increasingly turn to European AI alternatives — Mistral AI from France, Aleph Alpha from Germany — backed by genuinely sovereign cloud infrastructure rather than just sovereignty-branded American infrastructure, that’s European compute, European cloud, euros instead of dollars. The trajectory is slow, and the gap is real. But unlike a regulatory framework that exists purely on paper, Europe is now also building the physical and corporate plumbing to make the alternative actually usable, not just legally mandated.

Regulation doesn’t kill the Techno-Dollar. But it builds structural incentives to route around it. And structural incentives, given enough time to compound, reshape entire industries.

Worth being precise about the timeline here, though. Everything just described is real, and it’s accelerating. But Europe’s sovereignty push still sits several years behind American infrastructure at scale. NVIDIA still designs the chips that even Europe’s “sovereign” GPU clusters run on. AWS, Azure, and Google Cloud together still control roughly two-thirds to 70% of the European cloud market itself, sovereignty branding notwithstanding. OpenAI, Anthropic, and Google still lead on frontier model capability. Europe is building the alternative. It hasn’t yet built enough of it to shift where the centre of gravity sits this decade. That’s exactly why Scenario 1 — American dominance holding through the 2020s — remains the more likely near-term outcome, even as Europe’s longer-term trajectory points toward the more fragmented Scenario 2.

The Techno-Dollar loop needs the world to keep buying American AI. Regulation is quietly building the exit ramps.

Chapter 7: The Three Scenarios for the Techno-Dollar

Where does this leave us? Three roads, branching from here.

Scenario 1: The Techno-Dollar Succeeds — Most Likely This Decade

America keeps its lead. NVIDIA’s moat holds — Blackwell chips, then Rubin chips, each generation widening the gap a little further. OpenAI and Anthropic’s frontier models stay clearly ahead of Chinese alternatives. The EU AI Act raises compliance costs, but doesn’t dislodge American AI from its perch.

Global AI demand keeps flowing through the dollar. By 2030, the AI market hits an estimated $1.2-2.5 trillion — almost entirely dollar-denominated. The petrodollar of the 21st century, real and running.

What makes this likely: NVIDIA’s Q1 FY2027 revenue — $81.6 billion in a single quarter, up 85% year-on-year — says the moat is still wide. American hyperscalers are pouring $500 billion-plus into AI infrastructure, Project Stargate alone accounting for a huge slice of it. The lead is real, and it’s not closing fast.

Scenario 2: The Fragmented AI World — Most Likely Long-Term

The efficiency tricks DeepSeek demonstrated first start spreading everywhere. Mistral strengthens in Europe. Qwen and other Chinese models mature. India, Korea, the UAE all start building competitive models of their own. China’s stack matures further and gets exported across the Global South.

Picture the world splitting into regional AI ecosystems instead of one global one: American AI for the West, Chinese AI for China and its Belt and Road partners, European AI for GDPR-sensitive work, Indian AI for South Asia. Each ecosystem settling its compute transactions in its own currency. The dollar’s AI demand doesn’t vanish — it just stops being the only game in town.

This is roughly what already happened with mobile phones, as a rough illustration rather than a precise figure: America invented the smartphone operating system, but today Android runs on Chinese hardware across a large share of the world — generating far less direct dollar demand than you’d expect, even though Chinese manufacturers still import machinery, tap dollar-denominated financing, and interact with dollar-based trade systems somewhere along their own supply chain.

Scenario 3: The DeepSeek Cascade — Low Probability, High Impact

Efficiency keeps improving, exponentially this time. By 2027-28, you can run frontier AI on commodity hardware — the same way smartphones eventually displaced mainframes.

If AI compute gets cheap enough that NVIDIA chips stop being the bottleneck, the dollar demand built on top of them collapses with it.

The Techno-Dollar was real. It was just shorter-lived than the Petrodollar.

What makes this unlikely soon: the jump from where models stand today to true commodity-level AI is still a big one. But the direction of travel — toward cheaper compute, not more expensive — points exactly this way.

For countries caught between American and Chinese AI ecosystems, these three scenarios aren’t an abstract debate. They’re a practical, near-term policy decision — and few countries face it more directly than India.

Key takeaway

American dominance is the most likely outcome this decade; a fragmented, multi-currency AI world is the more likely outcome long-term.

Chapter 8: What This Means — For India, For the World

Here’s where the abstraction turns concrete.

If the Techno-Dollar fully takes hold, the path looks like this: the dollar stays strong. India’s import bill — oil, chips, AI services, all priced in dollars — stays high. The rupee stays under pressure. The current account deficit stays sticky.

If the Techno-Dollar partially fragments, the path bends differently: India gets more pricing power. Indian AI companies — Sarvam AI, Krutrim, others emerging behind them — may be able to serve the domestic market in rupees instead. India’s compute import bill could end up partly denominated in non-dollar currencies.

India’s position here is genuinely interesting, because it’s caught between both futures at once.

India is building its own AI ambitions — the IndiaAI Mission, investment in domestic compute, homegrown models. If that bet pays off, it could meaningfully reduce India’s dollar demand from AI. But today, India still builds mostly on American infrastructure — which means every AI token generated inside India is, right now, a dollar earned by America.

So the policy choice comes down to two roads. Build domestic AI infrastructure, and reduce dollar dependency over time. Or import American AI, pay in dollars, and risk deepening dependence on dollar-denominated infrastructure.

That second road isn’t simply the worse one, and the real tension here isn’t “good for India versus bad for India” — it’s something sharper: productivity gain now versus monetary sovereignty later. Importing American AI could genuinely make Indian companies more productive, more competitive in global services exports, more capable of earning dollars in return. That’s a real upside, not a footnote. But it doesn’t cancel the other side of the ledger — it cements dependency on dollar-denominated infrastructure for every future intelligence task India runs through it. Both things are true at once: growth now, and a deeper reliance on someone else’s currency later. That’s the actual trade India is making, whichever way the economics nets out.

This isn’t hypothetical. It’s the live policy debate happening in South Block today.

The Treasury Test

Before closing, one question cuts through everything this article has argued.

If NVIDIA’s revenue doubled again tomorrow, would that automatically create twice as many buyers for US Treasury bonds?

Almost certainly not.

This is the blunt version of the recycling-versus-reinvestment distinction from Chapter 3, and it deserves to be said plainly, not softened into a footnote. Reserve currency dominance was never really about how much of the world’s shopping happens in dollars. Boeing, Apple, and Microsoft have generated enormous dollar revenue for decades, and nobody calls the dollar’s dominance the “Boeing-Dollar” or the “iPhone-Dollar.” What actually anchors a reserve currency is debt markets — who buys the bonds, who holds the collateral, who needs the currency not just to spend, but to save and lend.

The Petrodollar worked because Saudi Arabia’s oil surplus had nowhere else trustworthy to go except US Treasuries — at scale, for decades, automatically. That automatic recycling is exactly what let America run growing deficits without paying a matching price in borrowing costs.

NVIDIA’s $216 billion in revenue doesn’t work this way. It funds stock buybacks, engineer salaries, the next generation of chips — strengthening American equity markets, not the Treasury market that actually has to absorb a $39 trillion and growing debt load.

This is why the honest conclusion isn’t that the Techno-Dollar is the next Petrodollar.

It’s a supplement, not a replacement. A genuinely significant new source of demand for dollars — just running through a different channel than the one that mattered most last time.

Conclusion: Not the Same River — A New Tributary

1973.The oil shock hit. By 1974-75, a relationship had taken shape in Riyadh. Oil in dollars.

1974.No deal needed. AI increasingly in dollars.

The Petrodollar was built on physical scarcity at every layer — you couldn’t manufacture oil, and you couldn’t fake having it. The Techno-Dollar is built on a more fractured foundation: physical scarcity at the hardware layer, and something far more fragile underneath, at the software layer.

The chips are hard to replicate — that part holds, for now. The models aren’t. DeepSeek showed that the software layer can be reverse-engineered, compressed, and rebuilt at a fraction of the cost, which means the Techno-Dollar’s weakest point was never America’s silicon. It’s the assumption that owning the best model matters as much as owning the best fab.

DeepSeek exposed the cracks in the wall. China is building a door through the software layer while it keeps catching up on hardware. Europe is legislating alternatives. India is still deciding which path to take.

This is structural support, not a cyclical driver — and it’s already working. A huge share of global AI hardware spending, every GPT-4o API call made in Nairobi or Jakarta or São Paulo, every Microsoft Azure AI deployment in Tokyo — these are all dollar demand events that the Petrodollar’s architects never imagined.

Scale matters here, and it’s worth being honest about it. Global FX markets turn over roughly $9.6 trillion every single day. The US Treasury market alone has more than $30 trillion outstanding, trading over $1 trillion daily. Set against numbers like that, NVIDIA’s entire FY2026 revenue of $216 billion — extraordinary as it is for one company — is a rounding error. AI’s importance to the dollar story was never about its current size. It’s the growth rate, and the fact that it’s one of the few genuinely new sources of dollar demand showing up at a moment when several older sources are weakening at once.

But two findings from earlier in this piece should pull on the brakes a little, before that claim travels too far.

First: the Treasury Test, above, already showed that AI profits don’t recycle into US debt the way petrodollars did — a gap that’s missing exactly the mechanism that made the original Petrodollar matter as much as it did.

Second: in the exact period this article covers, the dollar didn’t get stronger. The DXY had its worst H1 performance in 50 years, in the same window NVIDIA’s revenue was setting records. What this points to is a structural force underneath a much larger cyclical decline — not a force strong enough to override Fed policy, tariffs, and deficit worries on its own.

Put those two findings side by side, and a more honest conclusion takes shape: the Techno-Dollar isn’t currently strong enough to keep the dollar dominant by itself, and it doesn’t fund America’s debt the way the Petrodollar did. What it may be doing instead is supplying a new source of demand at the exact moment several older sources are fading — a floor, not a foundation.

And that’s not a contradiction of the earlier point about NVIDIA’s revenue being a rounding error against Treasury and FX market size. Think of it this way: small flows can still matter at the margin — not because they can replace the dollar’s existing support structure, but because they can slow how fast it erodes. A rounding error against a $30 trillion Treasury market can still be the difference between a 9% annual dollar decline and an 11% one. At that scale, a gap that small compounds into something real over a few years.

AI is not oil.

AI is software. Software copies. Software improves. Software spreads. The hardware layer holding up today’s Techno-Dollar is genuine — but it’s a thinner foundation than the physical scarcity that held up the Petrodollar for half a century.

Will the Techno-Dollar become the most significant extension of dollar dominance since Bretton Woods? Or a shorter-lived structural support that fades as compute gets cheaper and the world builds its own alternatives? The evidence inside this article points toward something more modest, and more defensible, than either extreme.

The Techno-Dollar is not the next Petrodollar. It doesn’t recycle into Treasuries the way oil money did. It can’t yet override a determined cyclical decline in the dollar. And the hardware moat it leans on sits on top of a manufacturing chokepoint in Taiwan that America doesn’t control.

What it is, more precisely, is a significant new source of structural dollar demand — arriving right as several of the dollar’s older supports weaken at the same time. Whether it ranks above or below stablecoins, eurodollar market expansion, or Treasury collateral demand in actual scale isn’t something this article can prove. No comparison of that kind was attempted here. That’s a smaller claim than “AI saves dollar dominance.” It’s still a more interesting one, and a harder one to wave away, than dismissing AI’s monetary role entirely.

How much this new source ends up mattering won’t be decided in Washington or on Wall Street. It’ll be decided in a server farm in Hangzhou, a fabrication plant in Hsinchu, a regulation committee in Brussels, and a policy decision in New Delhi.

Strip away every caveat in this article, and one plain sentence is still standing underneath all of them: the Techno-Dollar is real, it is meaningful, and it is not powerful enough to replace the Petrodollar. Not a sequel. Not a rebrand of an old cloud story. A new tributary feeding into the dollar’s dominance — smaller than the river it’s joining, but large enough, and growing fast enough, that no honest account of the dollar’s future from here can leave it out.

Not the same river. A new tributary — meaningful, but it doesn’t replace the main channel, and it draws from sources America doesn’t fully control.

One more thread, for another day. The Petrodollar exported dollars through oil. The Techno-Dollar exports dollars through compute. Stablecoins may represent a different path for dollar expansion entirely — one worth examining separately.

Claim

Verdict

TSMC has been legally barred from supplying Huawei since September 2020

✅ Confirmed — both companies publicly stated this

Huawei obtained ~2-3 million Ascend chip dies from TSMC via shell companies (Sophgo, PowerAir) between 2023-2024, without TSMC’s knowledge of true end-use

TSMC fabricates effectively all of NVIDIA’s leading-edge chips

✅ Confirmed — NVIDIA is fabless, relies on TSMC for advanced nodes

NVIDIA FY2025 full-year revenue $130.5 billion, up 114%

✅ Confirmed — NVIDIA official earnings Feb 2025

NVIDIA FY2026 full-year revenue ~$216 billion (official: $215.9B), up 65%

✅ Confirmed — NVIDIA official earnings Feb 2026

DXY (dollar index) fell ~10-11% in H1 2025, worst H1 performance in 50+ years

✅ Confirmed — JPMorgan, Morgan Stanley, multiple sources

DXY fell ~9.6% for full year 2025

✅ Confirmed — Barchart/multiple sources

Morgan Stanley called H1 2025 the end of a 2010-2024 structural dollar bull cycle

✅ Confirmed — Morgan Stanley Research

DeepSeek released V4 (V4-Pro, V4-Flash) on April 24, 2026, optimized for Huawei Ascend chips

✅ Confirmed — Reuters, multiple sources

DeepSeek V4 gave Huawei/Chinese chipmakers exclusive early access, excluding NVIDIA/AMD

✅ Confirmed

DeepSeek V4 “trained entirely on Chinese silicon”

⚠️ Disputed — training origin contested; NVIDIA ran V4-Pro on its own Blackwell chips same-day, Tsinghua professor says likely mainly NVIDIA-trained, US official alleged smuggled Blackwell use (denied by DeepSeek)

DeepSeek R2 was never formally released; reportedly shelved by CEO decision

✅ Confirmed — Reuters reporting, mid-2025

Formal US-Saudi dollar-oil pricing arrangement generally dated to 1974-75, not 1973 (1973 was the oil embargo/price shock)

✅ Historians’ consensus — 1973 marks the embargo, not the formal arrangement

Global oil market trades roughly $2-3 trillion annually

✅ Confirmed — approximate range across multiple industry sources, varies by year/price

Saudi Arabia historically recycled petrodollar surplus into US Treasury bonds

✅ Confirmed — well-documented pattern since 1970s, though exact mechanisms have evolved

NVIDIA Q1 FY2027 revenue $81.6 billion, up 85% YoY

✅ Confirmed — NVIDIA official earnings, May 20, 2026

US dollar on one side of 89.2% of all global FX trades (April 2025)

✅ Confirmed — BIS Triennial Survey 2025

DeepSeek-V3 base model cost ~$5.6M (2,048 H800 GPUs, ~55 days)

✅ Confirmed — community estimate from disclosed GPU-hours in DeepSeek’s technical paper

DeepSeek R1 API 96% cheaper than OpenAI o1 per token

✅ Confirmed — $0.55/M vs $15/M input tokens

NVIDIA lost ~$600B market cap in single day after DeepSeek

✅ Confirmed — January 27, 2025

Global AI market ~$294-390B (2025, estimates vary by methodology)

✅ Confirmed — Grand View Research, Fortune Business Insights

Global AI market projected $1.2-2.5T by 2030

✅ Confirmed — multiple research firms

North America accounts for ~35% of global AI market

✅ Confirmed — Grand View Research 2025

Italy temporarily banned ChatGPT March 2023

✅ Confirmed — Italian DPA (Garante)

EU AI Act enacted 2024 — world’s first comprehensive AI regulation

✅ Confirmed

DeepSeek R1 launched January 2025, became most downloaded app on US iOS App Store

✅ Confirmed

Project Stargate — $500B AI infrastructure commitment, OpenAI/SoftBank/Oracle

✅ Confirmed — announced January 2025

Ugaateyraho | Keep learning. Keep growing.[Read the full Dollar Story series: Part 1 → Part 2 → Part 3 → Part 4]

FAQ

What is the Techno-Dollar?

The idea that American AI dominance creates the kind of structural global dollar demand that Saudi oil once created through the petrodollar system in the 1970s. NVIDIA chips, AWS compute, OpenAI APIs — nearly all priced in dollars, regardless of where in the world the buyer sits. The underlying resource changed from energy to intelligence. The currency at the centre of it didn’t. Even when a payment is invoiced in euros or another local currency, it usually still creates dollar demand somewhere upstream — most country-pair currency markets lack direct liquidity, so cross-border payments route through the dollar as a “vehicle currency,” the role it played in 89 % of all global FX trades in the BIS’s most recent (2025) Triennial Survey.

Is AI actually strengthening the US dollar — and why did the dollar fall so much in 2025 if it is?

AI creates structural dollar demand — NVIDIA’s roughly $216B FY2026 revenue proves it. But the dollar still fell 10-11% in H1 2025. Two forces at work: cyclical pressures (Fed cuts, tariffs, debt concerns) versus structural AI demand. The latter may slow the decline, not reverse it. Full breakdown in Chapter 3.

Is the Techno-Dollar really the same as the Petrodollar?

Not quite, and the difference matters — this is the Treasury Test from the article. The Petrodollar worked because Saudi oil surplus was automatically recycled into US Treasury bonds, funding America’s deficit directly for decades. NVIDIA and Microsoft’s AI profits don’t do this — they fund stock buybacks, salaries, and more chips, not Treasury purchases. If NVIDIA’s revenue doubled tomorrow, it wouldn’t automatically create more buyers for the $39 trillion in US debt. The more accurate framing: the Techno-Dollar is not the next Petrodollar, but a significant new source of structural dollar demand — a supplement, not a replacement. Whether it’s larger or smaller than stablecoins or eurodollar market growth in actual scale isn’t something this article attempts to settle.

Does TSMC undermine the Techno-Dollar thesis?

It’s the single biggest structural hole in it. NVIDIA designs chips but doesn’t manufacture them — Taiwan Semiconductor Manufacturing Company (TSMC) fabricates roughly 90% of the world’s most advanced logic chips, including effectively all of NVIDIA’s leading-edge silicon. America’s compute dominance ultimately rests on Taiwanese manufacturing capacity, located roughly 180 kilometres from a country that has stated its intent to reunify with Taiwan, by force if necessary. A serious disruption to TSMC would shake the Techno-Dollar harder than DeepSeek or EU regulation ever could, because it would constrain the supply of compute itself, not just its price or origin. Worth noting: TSMC has been legally barred from supplying Huawei specifically since 2020, and Taiwan closed a 2023-24 shell-company loophole in 2025 — so this chokepoint cuts against China’s chip ambitions too, not just America’s.

Did DeepSeek kill the Techno-Dollar — and is China actually building a dollar-free alternative?

Not killed — cracked, and the crack has widened since. In January 2025, markets reacted to DeepSeek’s disclosed ~$5.6 million base-model cost (DeepSeek-V3) — wiping $600 billion off NVIDIA’s market cap in a single day, the largest single-day loss in stock market history. (The now-famous $294,000 figure, covering just R1’s reinforcement-learning layer, wasn’t actually disclosed until a Nature paper in September 2025 — eight months later, so it wasn’t part of the original shock.) Combined, the realistic total training cost is an estimated $5.9 million — still roughly 1/100th of GPT-4’s reported $600 million+. That crack widened further on April 24, 2026, when DeepSeek released V4 and gave Huawei exclusive early optimization access, shutting NVIDIA and AMD out entirely. Whether V4 was actually trained on Chinese silicon remains disputed — a US official alleged smuggled NVIDIA Blackwell chips, DeepSeek denies it, a Tsinghua professor suggested it may still have been mainly NVIDIA-trained — but the exclusive access and inference deployment to Huawei is verified, and is a meaningful proof point for China’s dollar-free ambitions regardless. Add Alibaba Cloud, Tencent Cloud, and Huawei Cloud, all fully yuan-denominated, and the picture is clear: American AI dominance is no longer the only option in the world. It’s still the leading one — NVIDIA’s FY2026 revenue of $216 billion proves demand remains massive — but DeepSeek opened a door that isn’t closing.

What does this mean for India?

India faces a real trade-off, and it isn’t simply good-versus-bad. Building AI on American infrastructure (AWS, Azure, NVIDIA) could make Indian companies more productive and more competitive in dollar-earning services exports — a genuine upside. But it also means every AI transaction India runs through that infrastructure deepens dependency on dollar-denominated systems for the long run, keeping pressure on the rupee. Building domestic AI infrastructure instead — the IndiaAI Mission, Sarvam AI, Krutrim — could reduce that dependency over time, at the cost of slower near-term gains. The real choice isn’t growth or sovereignty. It’s growth now versus sovereignty later, and India hasn’t settled which it wants more.

From the Nixon Shock to the 2025 Tariffs — Why Does India Keep Paying the Bill for Someone Else’s Emergency? Prologue: My Game, My Rules We all remember that one kid from the neighbourhood cricket match who owned both the bat and the ball. As long as he was winning, everything was fine. Standard rules….

The 2008 Crisis, Money Printing, Bitcoin, and the Rebellion Against Dollar Dominance [← Read Part 2: Dollar Story Part 2 — How the Dollar Became King] Quick Answer — What’s in This Article? What was the 2008 financial crisis? A global financial meltdown triggered by the collapse of the subprime mortgage market — Bear Stearns,…

America Ka Debt, Gold Ki Wapasi, Stablecoins Ka Raaz Aur Dollar Ke Teen Possible Futures [← Part 3 padhne ke liye yahan click karein: Dollar Ki Kahani Part 3 — Jab Dollar Ka Dil Rukne Wala Tha] Quick Answer — Is Article Mein Kya Milega? Dollar marega kya? Nahi — lekin badlega zaroor. Koi bhi…

2008 Crisis, Money Printing, Bitcoin Aur Dollar Ke Khilaaf Shuru Hui Baghawat [← Part 2 padhne ke liye yahan click karein: Dollar Ki Kahani Part 2 — Dollar King Kaise Bana] Quick Answer — Is Article Mein Kya Milega? 2008 financial crisis kya tha? Subprime mortgage collapse se shuru hua ek global financial meltdown —…

Quick Answer: An investment bank helps companies raise money, advises on mergers, and trades securities. It does not take deposits. A bank holding company is a parent corporation that owns banks and multiple financial businesses, has access to deposit-based funding, and operates under stricter federal regulation. The key difference: how they are funded, and what…

“This article is also available in Hinglish — Dollar Ki Kahani Part 1 padhne ke liye yahan click karein” How a Broke Young Country Created the World’s Most Powerful Currency Today, the US dollar feels almost untouchable. Oil is priced in it. Global trade runs through it. Countries hold it in reserves. And whenever there’s…

One Comment

Outstanding article! The comparison between the Petrodollar and the emerging Techno Dollar is both innovative and insightful. It brilliantly highlights how AI, semiconductors, cloud infrastructure, and digital ecosystems may become the strategic assets of the next economic era. 👌

Outstanding article! The comparison between the Petrodollar and the emerging Techno Dollar is both innovative and insightful. It brilliantly highlights how AI, semiconductors, cloud infrastructure, and digital ecosystems may become the strategic assets of the next economic era. 👌