From the Nixon Shock to the 2025 Tariffs — Why Does India Keep Paying the Bill for Someone Else’s Emergency?

Prologue: My Game, My Rules

We all remember that one kid from the neighbourhood cricket match who owned both the bat and the ball.

As long as he was winning, everything was fine. Standard rules. Proper cricket. Very civilised.

But the moment he was about to get out — suddenly, mysteriously, the rules changed.

“That ball was just a trial ball.”

“No LBW today.”

“It’s my bat, so I’m taking it home.”

Everyone hated it. Everyone kept playing. Because there was no alternative.

In the grand stadium of the global economy, the United States has — at certain crucial moments — behaved exactly like that kid.

Not out of malice. Not always out of arrogance. Often simply out of one very specific instinct: when the rules stop working for us, we change the rules.

The world saw this most dramatically in August 1971, when Nixon ended the gold standard in a Sunday night TV speech — without warning, without consultation, without apology.

It saw it again in April 2025, when Trump declared “Liberation Day” and slapped tariffs on virtually every country on Earth — erasing $6.6 trillion in global market value in the two days following the announcement, before a partial recovery after a 90-day tariff pause.

Different presidents. Different crises. Same logic: America in pain, acting alone, leaving the bill on everyone else’s table.

Quick Answer

The Nixon Shock (1971) and Trump’s Liberation Day tariffs (2025) are two of the most consequential unilateral economic decisions in modern history — both made by the United States without consulting the world, both triggered by domestic pain, and both leaving other countries to absorb the consequences. Nixon closed the gold window and ended the Bretton Woods monetary system in a single Sunday night speech. Trump announced sweeping tariffs on virtually every country, erasing $6.6 trillion in global market value in the two days following the announcement, before a partial recovery after a 90-day tariff pause.

- Nixon Shock (1971): Ended the dollar’s gold convertibility, collapsed the Bretton Woods system, shifted the world to floating exchange rates — permanent and irreversible.

- Trump Tariffs (2025): Universal import tariffs under emergency powers, partially struck down by the Supreme Court in 2026 — disruptive but reversible.

- Key difference: Nixon faced a structural impossibility (the Triffin Dilemma). Trump is fighting a trade deficit that dollar dominance structurally requires.

- India’s position: In both cases, India had no vote but paid the price — currency volatility in 1971, export losses of up to $48.2 billion at risk in 2025.

This Is Not Trump’s First Match

Before the Nixon comparison — a clarification. Trump used tariffs in his first term too. Steel, aluminium, a China trade war. Loud, disruptive, politically effective.

But that doesn’t qualify for the Nixon comparison. Here’s why.

First-term Trump was targeted and negotiated — it ended in a Phase 1 deal with China. What happened in 2025 was categorically different.

| Trump Term 1 (2018–19) | Trump Term 2 (2025) | |

|---|---|---|

| Scope | China + steel/aluminium | Near-universal — all countries, all goods |

| Legal basis | Standard trade statutes | IEEPA emergency powers — legally untested |

| Scale | ~$380 billion in imports | ~$1.4 trillion in global trade |

| Market impact | Significant but absorbed | $6.6 trillion erased at peak (partial recovery after 90-day pause) |

| Shock character | Gradual escalation | Single announcement, global panic |

Term 1 was a trade dispute. Term 2 was a system-level shock. When we say “Trump tariffs” in this article, we mean Liberation Day 2025.

Act I: What Was the Bretton Woods System?

To understand what Nixon did, you need to go back to 1944 — a luxury hotel in New Hampshire, forty-four nations, and one enormous ambition: build a financial system stable enough to prevent another Great Depression- the full story of how the dollar rose to power is covered in our Dollar : The Birth of an Empire – Part 1

The Bretton Woods system, established in July 1944, was a global monetary framework in which every major currency was pegged to the US dollar, and the dollar itself was convertible to gold at a fixed rate of $35 per ounce. Any country holding dollars could exchange them for gold at any time. America was the anchor. The promise was absolute.

For two decades, it worked beautifully. Global trade expanded. Europe rebuilt. Japan industrialised at breathtaking speed. And at the centre of it all sat the dollar, quietly accumulating the world’s trust.

But a Belgian-American economist named Robert Triffin saw the problem coming from miles away.

What Is the Triffin Dilemma — And Why Does It Still Matter?

In 1960, Triffin walked into the US Congress and explained what would become known as the Triffin Dilemma: the fundamental contradiction built into being the world’s reserve currency issuer.

His argument, in plain terms: for the world to grow, it needed dollars. The only way to supply those dollars was for America to run persistent trade deficits — spending more abroad than it earned. But the more dollars piled up in foreign hands, the less believable America’s gold promise became. You can’t keep printing dollars and keep promising gold. Eventually, someone calls your bluff.

The Triffin Dilemma still matters today because it explains why Trump’s tariffs are fighting something America structurally needs. To supply the world with dollars, the US must run trade deficits. Trump’s anger about the trade deficit is, in a very real sense, anger about the price of dollar dominance — a price Nixon’s 1971 decision helped create and deepen.

I find this one of the most elegant — and brutal — ideas in all of economics. A man tells the most powerful government on Earth that their financial system has a fatal design flaw, gets politely thanked, and is ignored for eleven years. Then the system collapses exactly the way he said it would. Nobody names anything after him in school textbooks. That’s how the world works. If you want to understand how the dollar weaponised this collapse to its own advantage, read The Dollar Story — Part 2.

Through the late 1960s, the cracks widened. Vietnam was draining the treasury. Dollars were flooding foreign central banks. France — furious at what de Gaulle called America’s “exorbitant privilege” — didn’t just complain in speeches. In 1965, de Gaulle sent an actual warship to New York to physically collect French gold.

That is not a metaphor. That is a warship. Carrying gold. Out of New York.

By 1971, according to Federal Reserve historical records, America’s gold reserves had fallen from roughly 20,000 tonnes in the late 1940s to approximately 8,000 tonnes. When Britain asked to convert $3 billion in dollars to gold — nearly a quarter of what America had left — the moment of reckoning had arrived.

Act II: What Exactly Was the Nixon Shock of 1971?

Nixon did not call a summit. He did not warn allies. He did not consult markets.

He gathered a handful of advisors at Camp David over a single secret weekend — the press was told it was a routine domestic policy meeting — and on Sunday evening, August 15, 1971, he went on national television.

The Nixon Shock refers to three simultaneous announcements made by President Richard Nixon on August 15, 1971: a 90-day freeze on wages and prices, a 10% tariff surcharge on all dutiable imports, and — most consequentially — the immediate suspension of the dollar’s convertibility into gold, effectively ending the Bretton Woods system. The measures were announced without prior consultation with allied nations or international institutions.

The gold window was closed. Just like that.

Foreign governments could no longer arrive with dollars and leave with gold. The promise at the heart of Bretton Woods — twenty-seven years old — was void. Nixon called it temporary. The gold window never reopened.

The world woke up Monday morning to discover the rules had changed. They hadn’t been consulted. They hadn’t been warned. They hadn’t been given a choice.

US Treasury Secretary John Connally met the objections of allied nations with a line I think about often: “The dollar is our currency, but it’s your problem.”

Honestly? That line infuriates me every time I read it. Not because it’s arrogant — it is — but because it’s so completely, brutally honest. Connally didn’t dress it up. He just said the quiet part out loud: the dollar belongs to America, the consequences belong to everyone else. Take it or leave it.

The problem is — you can’t leave it. That’s exactly the point.

Act III: Liberation Day and the Geopolitics of American Anxiety (April 2, 2025)

Fast forward fifty-four years.

America’s manufacturing had hollowed out. The Rust Belt had rusted. Trade deficits — the very thing the Triffin Dilemma said was structurally necessary for a reserve currency issuer — had become a political emergency. China had spent thirty years absorbing American investment and technology, and emerged as a near-peer competitor in semiconductors, electric vehicles, shipbuilding, and artificial intelligence.

But the anxiety in 2025 ran deeper than manufacturing. China’s yuan was slowly gaining ground in bilateral trade settlements. The BRICS nations — Brazil, Russia, India, China, South Africa, and new members — had been openly discussing alternatives to the dollar-dominated SWIFT payment system. Central banks worldwide, according to World Gold Council data, were buying gold at the fastest rate since the 1960s — a quiet but unmistakable vote of declining confidence in dollar-only reserves. America wasn’t just losing factory jobs. It was watching the foundations of its financial dominance develop hairline cracks.

This is the geopolitical context that made Liberation Day feel different from Term 1 tariffs. It wasn’t just a trade dispute. It was an assertion: we still control this system, and we will use that control aggressively.

Trump’s first-term tariffs hadn’t fixed any of it. China simply rerouted exports through Vietnam and Mexico. Biden kept the tariffs and changed little strategically.

By 2025, Trump’s diagnosis was starker: the entire global trading system was rigged against America, and only a universal shock would do.

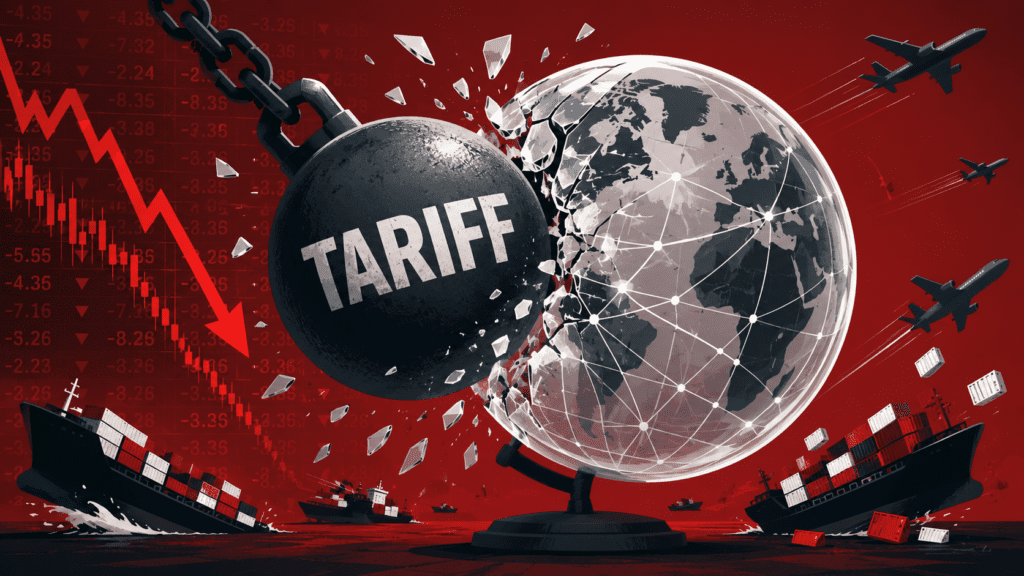

On April 2, 2025, he stood in the Rose Garden and announced a baseline 10% tariff on every country, with additional “reciprocal” rates on top — calculated on a formula that the Peterson Institute for International Economics described as methodologically unsound. China eventually faced tariffs exceeding 100%.

According to Reuters market data, $6.6 trillion in global market value was erased in the two days following the announcement — before a partial recovery after Trump announced a 90-day pause on some country-specific tariffs later that month. The dollar weakened. The WTO called it a crisis. The IMF cut growth forecasts.

Then the legal floor gave way. Trump had justified the tariffs under the International Emergency Economic Powers Act — a sanctions statute, never before used for tariffs. On February 20, 2026, the Supreme Court ruled 6-3 that IEEPA does not authorise tariffs. Trump responded within hours with a new 10% global tariff under a different law, signalling he’d push it to 15%.

According to the Tax Foundation’s 2025 Tariff Tracker, the average US tariff rate that year became the highest since 1947 — and for 2026, even after the Supreme Court ruling, it remained the highest since 1972. One year after Nixon.

Here’s my honest read: the grievance is real, but the tool is wrong. American manufacturing decline is genuine. China’s trade practices have been genuinely unfair. But a blanket tariff on every country — including allies, including countries with nothing to do with the trade deficit — is not a scalpel. It’s a sledgehammer. The early numbers show it: the trade deficit barely moved, China adapted faster than expected, and according to the Tax Foundation, American households are paying roughly $1,500 more per year. That’s not winning. That’s just expensive.

The Comparison: Where It Holds, Where It Breaks

What they share:

Both Nixon and Trump were responding to real economic pain — gold drain and inflation in 1971, trade deficits and deindustrialisation in 2025. Both acted alone, without consulting the institutions they had helped build. Both reached for the same trade weapon: Nixon’s package included a 10% import surcharge — almost nobody mentions this — identical in concept to Trump’s baseline tariff. And in both cases, global markets panicked immediately.

Where they differ — and this matters:

Nixon broke the architecture. Trump is working within it — mostly. Nixon ended a 27-year foundational agreement. There was no going back. Trump’s tariffs can be reversed, challenged, struck down in court. Which they were.

More importantly: Nixon faced a mathematical impossibility. The Bretton Woods system was always going to collapse — the Triffin Dilemma guaranteed it. Nixon was the one standing there when the clock ran out. His hand was forced.

Trump’s trade deficit, by contrast, is a structural feature of dollar dominance. The United States needs to run trade deficits to supply the world with dollars. You cannot simultaneously be the world’s reserve currency issuer and run a trade surplus. Trump is fighting the consequence of dollar dominance with a tool that makes dollar dominance more expensive to maintain. The irony would be funny if it weren’t so costly for everyone else.

What This Means for India

1971: The Anchor Disappears

Imagine waking up one morning and discovering that the exchange rate your entire trade and monetary policy was built around no longer exists — and nobody told you it was changing.

That’s essentially what happened to India in 1971. The rupee was pegged to the British pound, which was pegged to the dollar, which was pegged to gold. When Nixon cut the gold link, the entire chain snapped. India entered an era of currency volatility it hadn’t prepared for, absorbing the inflation and commodity price shocks of the 1970s with no reserve currency of its own to cushion the blow.

India did not make the decision. India lived with the consequences.

2025: A More Direct Blow

With Liberation Day, the hit was faster and more personal.

India’s initial “reciprocal” tariff was 26%. Lower than China’s 100%, lower than Vietnam’s 46% — which in a trade war counts as a relative advantage, the way being second-last in a collapsing building counts as lucky. But it was still 26%. And it was just the beginning.

Think about what a 26% tariff means for a diamond polisher in Surat whose entire livelihood depends on American buyers — India ships over a third of its diamond exports to the US. Or a textile worker in Tirupur whose factory has been running American orders for twenty years. Overnight, their products became significantly more expensive on their most important shelf. No warning. No consultation. Just a Rose Garden speech and a new number.

According to the Global Trade Research Initiative, India’s exports to the US were projected to fall by over 6% — nearly $5.76 billion — in 2025. And then it got worse.

By mid-2025, Trump escalated further, citing India’s purchases of Russian oil, and pushed tariffs on certain Indian goods to 50%. The Indian government estimated $48.2 billion in exports were now at risk. Some shipments, officials warned, would become “commercially unviable.”

This is the part that genuinely frustrates me. India buying Russian oil is a sovereign decision made in India’s national interest. Every country makes energy decisions this way — America buys Gulf oil, Europe bought Russian gas for decades. But when India does it, it becomes a tariff trigger. We get punished for a geopolitical choice that has nothing to do with bilateral trade. That’s not trade policy. That’s coercion dressed up in economics. And India, to its credit, did not blink — but our exporters paid the price regardless.

India chose not to retaliate. It reserved WTO rights quietly and started opening conversations with Latin America, Africa, and other markets — the first real signal of a deliberate pivot away from US dependence. Small steps. But the direction is right.

The Great Irony: Nixon Killed the System and Made the Dollar Stronger

Here’s the twist most people don’t know.

Everyone assumed ending the gold standard would weaken the dollar. The opposite happened.

Freed from the gold constraint, the dollar gained flexibility it never had before. Add America’s deep capital markets, its military reach, its institutional control of the IMF and World Bank — and then the petrodollar arrangement in the 1970s, where Saudi Arabia agreed to price oil exclusively in dollars — and the dollar emerged from the wreckage of Bretton Woods more dominant than it had ever been under the gold standard.

The system died. The dollar was promoted.

Nixon didn’t weaken the dollar. He accidentally freed it from the thing that was slowly killing it.

Whether Trump gets the same lucky outcome — the numbers so far are not encouraging. According to the Peterson Institute for International Economics, the trade deficit barely moved. China posted a record $1.1 trillion trade surplus in 2025, having rerouted supply chains faster than anyone expected. According to the Tax Foundation, US GDP is projected to be 0.3% smaller from the permanent tariffs alone.

Nixon rolled the dice and got lucky. Trump rolled the same dice. The numbers are still being counted.

My personal bet is that Trump won’t get Nixon’s outcome. Nixon solved a structural problem that had no other solution. Trump is trying to solve a political problem with an economic tool that economists broadly agree is the wrong one. The dice look the same. The game is not.

Key Takeaways

- The Nixon Shock (1971) ended the Bretton Woods gold standard in a single Sunday night speech, without warning to any allied nation. It was the most consequential unilateral monetary decision of the 20th century.

- Trump’s Liberation Day (2025) was a system-level shock — universal tariffs on all countries, $6.6 trillion erased in two days — that earns the Nixon comparison in a way that Trump’s first-term tariffs do not.

- The deepest parallel: both Nixon and Trump reached for tariffs as part of their economic announcements. Nixon’s 1971 package also included a 10% import surcharge — almost never mentioned in popular coverage.

- The deepest difference: Nixon faced a mathematical impossibility (Triffin Dilemma). Trump is fighting a structural feature of dollar dominance — the very trade deficit that allows America to supply the world with dollars.

- For India: both episodes confirm the same vulnerability — when you depend on a system you don’t control, someone else’s domestic emergency automatically becomes your economic problem.

- The geopolitical stakes in 2025 are higher than 1971 — China’s rise, BRICS currency discussions, and record central bank gold buying suggest the dollar’s dominance is under longer-term structural pressure for the first time since Bretton Woods.

The Ending: Someone Else’s System, Your Emergency

The Nixon Shock and Liberation Day were separated by fifty-four years.

Different presidents, different problems, different tools. But the same underlying reality: when the country at the centre of the global economy changes direction, everyone else must respond. No vote. No notice. The announcement comes on a Sunday evening or a Tuesday in a Rose Garden, and by the time the markets open, the world is different.

For India, the lesson from 1971 and 2025 is the same.

When you depend on a system you didn’t design and don’t control, someone else’s domestic emergency automatically becomes your economic problem. The mechanism changes — floating exchange rates one decade, punitive tariffs the next. The vulnerability doesn’t.

I’ll end with this: I don’t think America is evil. Nixon was trying to save his economy. Trump is trying to save his political base. Both are doing what powerful countries do — acting in their own interest, at scale, without asking permission. That’s not a conspiracy. That’s just power.

The question for India is not whether America will do this again. It will. The question is whether, the next time that Sunday night speech comes, we’ll be in a position where it’s their problem — and not automatically ours.

We’re not there yet. But we should be working towards it.

FAQ

Q: What was the Nixon Shock of 1971?

The Nixon Shock refers to President Nixon’s August 15, 1971 announcement suspending the dollar’s convertibility into gold, effectively ending the Bretton Woods international monetary system. The decision also included a 90-day wage and price freeze and a 10% import tariff surcharge. It was made without consulting allied nations and came as a complete surprise to global markets.

Q: What is the Triffin Dilemma in simple terms?

The Triffin Dilemma is the inherent contradiction in being the world’s reserve currency issuer: to supply the world with dollars, America must run trade deficits. But persistent trade deficits eventually undermine confidence in the dollar. You can’t supply the world’s currency and maintain a trade surplus at the same time. This is why Trump’s tariff war against trade deficits is, ironically, a war against a feature of dollar dominance — not a bug.

Q: How do Trump’s 2025 tariffs compare to the Nixon Shock?

Both involved unilateral American action that shocked global markets. Both included tariffs as part of the package — Nixon’s 1971 announcement also had a 10% import surcharge. The key difference: Nixon ended a 27-year architectural agreement with no going back. Trump’s tariffs, while historically large, operate within a framework that can be reversed, negotiated, or struck down — as the Supreme Court demonstrated in February 2026.

Q: Why didn’t ending the gold standard weaken the dollar?

Because the petrodollar system replaced gold as the dollar’s anchor. When Saudi Arabia agreed in the mid-1970s to price oil exclusively in dollars, global demand for dollars became structurally guaranteed regardless of gold backing. The dollar’s dominance deepened after 1971, not weakened — one of the great counterintuitive outcomes in modern economic history.

Q: How did Trump’s tariffs affect India specifically?

India faced a 26% initial reciprocal tariff, later escalated to 50% on certain goods over the Russian oil issue. According to the Global Trade Research Initiative, India’s US exports were projected to fall over 6% ($5.76 billion) in 2025. The government estimated $48.2 billion in exports were at risk after the escalation. India chose not to retaliate, instead quietly diversifying toward Latin American and African markets.

Q: Is dollar dominance under threat in 2026?

It’s under longer-term structural pressure, but not immediate threat. Central banks are buying gold at the fastest rate since the 1960s. BRICS nations are exploring alternative settlement systems. Some bilateral trade is settling in local currencies. But no credible alternative reserve currency exists today — the yuan, euro, and BRICS basket cannot absorb the dollar’s role. Gradual de-dollarisation is likely over decades. Sudden displacement is not.

Powerful and thought-provoking article. The Nixon Shock and 2025 tariff comparison is explained in a very simple yet impactful way. Especially the India angle makes it highly relevant — a strong reminder that countries must reduce dependence on systems they don’t control. Excellent writing!

Thanks Nishith!