Will the dollar die? No — but it will change. No dominant reserve currency dies overnight. The British pound still exists. The dollar will survive — but its court is changing around it.

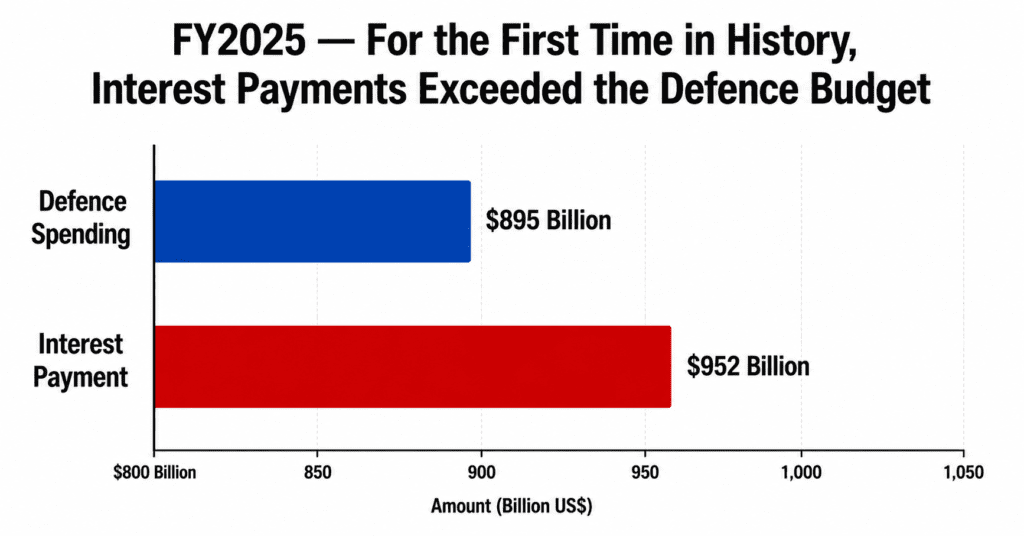

How serious is America’s debt? By late 2025 it had crossed $36 trillion — and by early 2026 it surpassed $39 trillion. Debt-to-GDP is estimated between 122-134% depending on methodology. FY2025 interest payments alone came to $952 billion — exceeding defence spending for the first time. Serious, not immediately catastrophic — but the trajectory is concerning.

Are stablecoins weakening the dollar? Exactly the opposite. The $300 billion stablecoin market is 80%+ backed by US Treasuries — making stablecoin issuers among the most significant buyers of American government debt globally.

What happens next? Three possible futures. The dollar survives in all three. Its role differs in each.

First, a Quick Recap

In Part 1 — the dollar’s birth. Bretton Woods. 44 nations. The gold guarantee.

In Part 3 — the dollar’s biggest test. The 2008 crisis. Quantitative Easing. Bitcoin’s birth. China’s chess move. Russia’s reserves frozen. De-dollarisation‘s practical beginning.

Now Part 4.

This is the biggest question of the entire series.

What is the dollar’s future?

Prologue: Every Empire Has Its Moment

Rome fell in 476 AD. But Roman law still lives inside Europe’s legal systems today.

The British Empire officially ended in 1947. But English is now the world’s lingua franca.

Empires never completely die. They transform.

The same question applies to the dollar. Not “will it die?” — but “how will it change?”

And to understand that change, we first need to look at the thing that seems boring but matters most.

America’s wallet. From the inside.

Chapter 1: America’s Wallet — What Nobody Wants to Look At

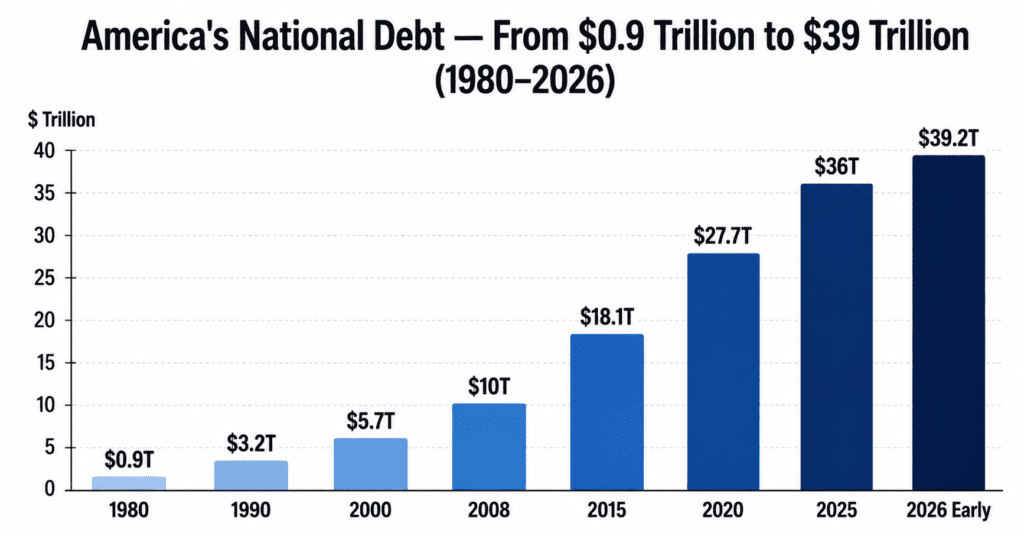

In 1980, America’s national debt was $900 billion.

Today?

By late 2025 it had crossed $36 trillion. By March 2026 — it had crossed $39 trillion too.

If this national debt were a country, it would be the world’s third-largest economy — surpassed only by the US and China.

Think of it this way: a household earns $100 a year. Their loan is $122. And every year they spend more than they earn — so the loan keeps growing.

Now imagine that household is the world’s most powerful. Their “money” is globally needed. So they don’t have to repay — the world keeps buying their debt anyway.

Total National Debt: $39.2 Trillion+ (as of June 2026 — was $36 Trillion in late 2025)

Debt-to-GDP Ratio: ~122-134% (source: FRED/OMB/Debt Clock data — estimates vary)

Annual Budget Deficit (FY2025): $1.8 Trillion

Annual Interest Payment (FY2025): ~$952 Billion

The Milestone: For the first time in history — US interest payments on past debt have officially exceeded the total national defence budget ($895 Billion).

Roughly one-third of India’s GDP. In interest payments.

And it’s only growing. The CBO’s projection: net interest payments over the next 10 years — $16.2 trillion.

Is this immediately catastrophic?

Honest answer: no.

Japan’s debt-to-GDP is ~260%. Japan is still functional. Why? Because most of Japan’s debt is held domestically — Japanese people buy their own government’s debt. They don’t depend on the outside world.

America’s debt is globally held. That means global confidence is required to sustain it.

It was symbolic. But symbols matter — especially when the world is already searching for alternatives.

Printing money “forever” can’t work — because confidence doesn’t last “forever.”

Chapter 2: The Dream of Killing the Dollar — A Graveyard Story

Every generation thinks the dollar is finished.

Every generation is proved wrong.

This chapter tells their stories.

1980s — The Japanese Yen’s Attack

Japan in the 1980s was rising like a rocket. Sony. Toyota. Panasonic. “Made in Japan” had become the world’s standard.

Experts declared: “The yen will replace the dollar. Japan will become the world’s #1 economy.”

In 1985 came the Plaza Accord — America, Japan, Germany, France, the UK — all jointly weakened the dollar deliberately to boost American exports. The yen dramatically appreciated.

Then what happened?

Japan’s real estate bubble burst in 1991. The “Lost Decade” began — which actually lasted two decades. The yen today trades at $1 = ¥150+. Whatever happened to replacing the dollar?

2000s — The Euro’s Challenge

The euro arrived in 1999. Notes and coins in 2002. All of Europe under one currency.

Experts declared: “The euro will overtake the dollar. Europe’s GDP is larger than America’s. The euro will become the reserve currency.”

In 2010 came the Greece crisis. Then Italy and Spain in 2011. Then Portugal. The ECB scrambled in emergency mode. Mario Draghi’s “whatever it takes” moment.

The euro survived. But becoming the #1 reserve currency? The dream stayed a dream.

The euro’s global reserve share today is still around ~20% — far behind the dollar’s 57%.

2010s — The Chinese Yuan’s Ambition

China became the world’s second-largest economy in 2010. Belt and Road. CIPS. Yuan internationalisation.

Experts declared: “The yuan will challenge the dollar by 2020.”

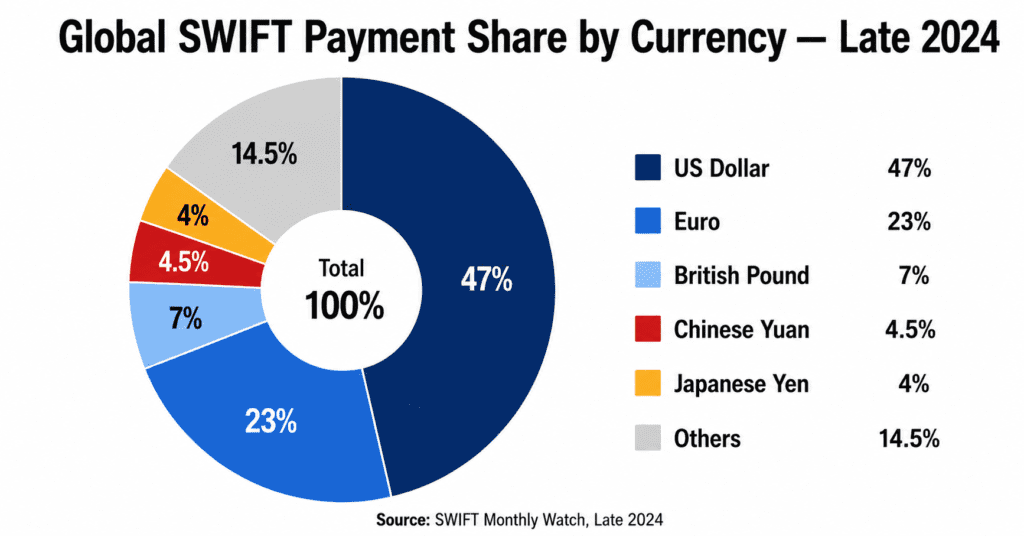

The yuan’s SWIFT global payment share in 2024? Roughly 4-5%.

The dollar’s? ~47%.

It never became a serious contender in the reserve currency race — why exactly, Chapter 3 will explain.

2020s — Bitcoin’s Rebellion

Satoshi created Bitcoin in 2009 — directly against the dollar system.

Bitcoin hit $60,000+ in 2020-21. Experts declared: “This is the end of fiat currency. The dollar will sink.”

Bitcoin is still alive — market cap in the trillions. Reserve currency? One tweet moves the price 30% in either direction. No serious economy runs on such a roller-coaster.

2024 — The BRICS Common Currency Hype

After the 2023-24 BRICS summit, social media erupted:

“BRICS currency is coming! Dollar finished!”

Reality: India and China have border tensions. Russia is under sanctions. Brazil has its own economic problems. Member countries have competing interests.

A common BRICS currency is still at the discussion stage.

The pattern is clear:

Every decade, a new “dollar killer” arrives. Every decade, it fails — or drowns in its own problems.

This doesn’t mean the dollar is invincible.

It means the world hasn’t yet built an alternative with the dollar’s depth, liquidity, and network effects.

The case against the dollar is weak — not because the dollar is perfect, but because the alternatives are even more imperfect.

But — and this “but” matters — the graveyard keeps filling up. One day someone will arrive who can’t be avoided.

Chapter 3: China vs Dollar — The 50-Year Game

One thing about China needs to be stated directly.

China will not remove the dollar tomorrow. Or the day after. Probably not even this decade.

But China is playing a 50-year game. And in a 50-year game, direction matters — not speed.

China’s Actual Progress:

Yuan’s SWIFT payment share (late 2024): roughly 4-5%. Dollar’s: roughly 47%. A massive gap. But in 2010, the yuan’s share was negligible — so the direction exists.

Source: SWIFT Monthly Watch, Late 2024.

What China Is Doing Practically:

Belt and Road + Yuan Settlement: Chinese infrastructure investment across 60+ countries, increasingly settled in yuan. Pakistan, Bangladesh, Sri Lanka, African nations — all have Chinese loans being settled in yuan.

CIPS Expanding: China’s Cross-Border Interbank Payment System now covers 200+ countries and territories. A SWIFT alternative — still small, but growing.

Commodity Pricing Experiments: Oil with Russia in yuan. Trade with Iran in yuan. Partial yuan trade with Brazil.

But the problem that won’t go away — Capital Controls.

An ordinary Chinese citizen can only take $50,000 in foreign exchange out of the country per year. The yuan is not freely convertible.

Why doesn’t China change this?

Because a freely convertible yuan would mean Chinese citizens could freely invest in dollars, euros, and gold — capital flight risk that the Communist Party has consistently chosen to avoid.

This is a political choice. And as long as this choice doesn’t change — the yuan cannot become the #1 reserve currency.

But China’s strategy isn’t just to make the yuan #1.

China’s real strategy is to limit the dollar’s “reach” and “leverage.” If trade increasingly happens in yuan, barter, or commodity settlements — the dollar’s leverage shrinks, even if the yuan doesn’t become dominant.

This is a subtler game. And China is clearly advancing in it.

One Hypothetical — The Single Biggest Game Changer:

If Beijing removed capital controls tomorrow — the world’s financial map would change overnight.

The yuan would become genuinely competitive. Global investors could freely invest in yuan. Chinese bonds, Chinese assets — all globally accessible. The yuan would become a serious contender in the reserve currency race overnight.

But the Communist Party has never done this. And the reason isn’t purely economic — it’s political.

A freely convertible yuan would mean 1.4 billion Chinese citizens could also freely take their money out of the country. Capital flight. The government’s economic control would begin to slip. The Party’s grip would loosen.

This isn’t an economic decision — it’s a survival decision.

As long as the Communist Party considers its power structure more important than that risk — the yuan will not directly challenge the dollar. China’s long game isn’t to remove the dollar. It’s to make the dollar irrelevant — gradually, without losing its own control.

Chapter 4: Gold — What We Forgot, What Is Quietly Returning

As tracked in Parts 1 and 2 — the 1971 Nixon Shock stripped gold from the system. Experts declared the gold era over. Fiat currency was the future.

50 years later, central banks are quietly putting it back.

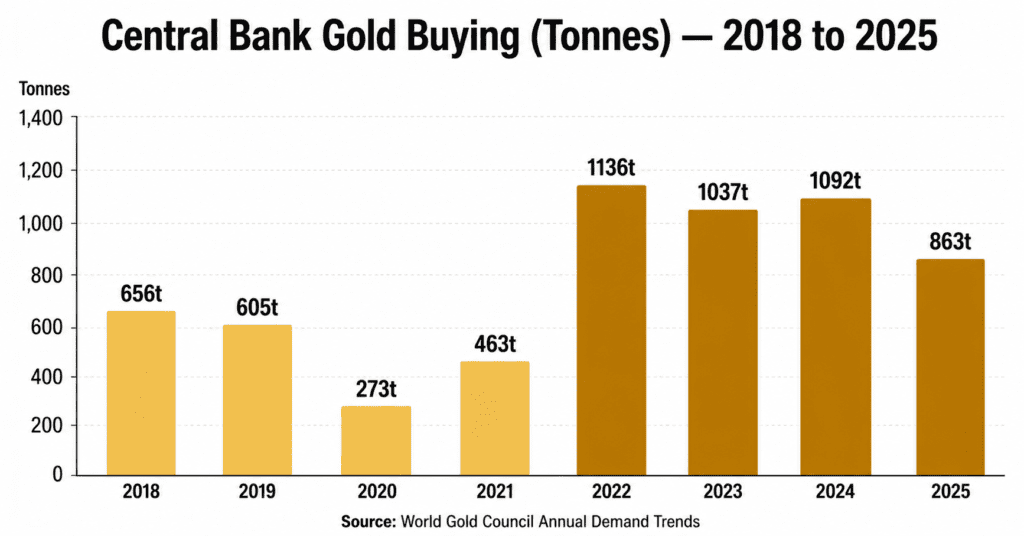

Gold’s 2022-2025 Story:

Year

Central Bank Gold Buying

2022

1,136 tonnes — highest since the 1950s

2023

1,037 tonnes — almost equally high

2024

1,092 tonnes — trend continuing

2025

863 tonnes — buying continues even at record prices

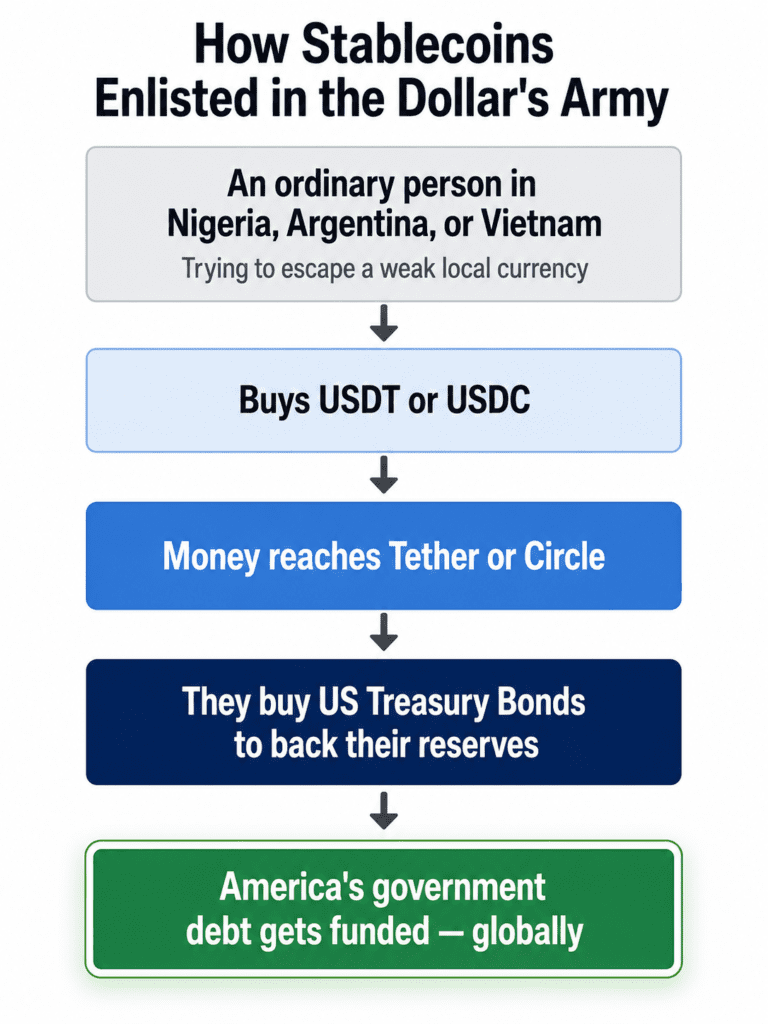

What is a Stablecoin? A cryptocurrency whose value is pegged to a stable asset — usually the US Dollar. 1 USDT is always ~$1. 1 USDC is always ~$1. Not volatile. Hence “stable” coin.

Now the numbers:

Stablecoin market cap by end of 2025: ~$300 billion+

USDT (Tether): ~$175 billion

USDC (Circle): ~$100+ billion

Where is this $300 billion backed from?

Mostly US Treasury bonds.

Tether and Circle primarily buy short-term US government debt to back their stablecoins. According to Brookings Institution’s 2025 analysis — Tether and Circle’s combined Treasury exposure by end of Q2-2025 was $177.6 billion.

This means — stablecoin issuers have become significant buyers in the US Treasury market — some estimates place them among the top 10 purchasers of US government debt.

Think about the dramatic implication:

Someone in Nigeria buys USDT to escape their naira’s inflation.

A trader in Argentina keeps savings in USDC to escape the peso.

A freelancer in Vietnam receives international payments in USDT.

Every time these people buy USDT or USDC — Tether and Circle use that money to buy US Treasuries.

[FLOWCHART — “How Stablecoins Enlist in the Dollar’s Army”]

The dollar’s reach is extending through crypto to people that traditional banking never reached.

In those countries — where local currencies are weak — people want dollars. They get digital dollars — USDT, USDC. And in this process, America’s government debt gets funded globally.

This is not the dollar weakening.

This is the dollar’s new weapon.

And America is officially embracing this weapon.

In 2025, serious steps toward the Stablecoin Genius Act — US-regulated stablecoins made mandatory to be 1:1 dollar-backed. The government is officially making stablecoins part of the dollar system.

The crypto community thought this was revolution.

The end result: the dollar’s digital empire is expanding.

But this digital empire has another face — one that isn’t quite as reassuring.

Chapter 6: CBDCs — When the Government Holds the Keys to Your Wallet

Imagine waking up one morning. You pick up your phone. Open the banking app.

There’s a message:

“Your wallet has been temporarily restricted. Please appeal within 48 hours.”

No number to call. No reason given. No branch to visit.

Today this is just imagination.

After CBDCs — it becomes a real possibility.

What is a CBDC (Central Bank Digital Currency)? A digital currency issued directly by a central bank. Legal tender like a physical note — but entirely digital. No intermediary bank — straight from the central bank into your wallet.

The State of CBDCs Globally:

Country

Status

China (e-CNY / Digital Yuan)

Pilot ongoing — hundreds of millions of users

India (Digital Rupee)

RBI pilot since 2022, expanding

Europe (Digital Euro)

Design phase — target 2027-28

USA (Digital Dollar)

Research only — politically blocked

Bahamas, Jamaica, Nigeria

Already launched

China’s e-CNY — Most Advanced and Most Revealing:

China has been running a digital yuan pilot since 2020. Multiple cities. Retail transactions. Used at the Olympics. But one feature that has been tested is particularly interesting:

Programmable money.

This means — the e-CNY technically allows the government to set an “expiry date” on specific wallet funds. Money must be spent within 6 months — or it cancels.

Or it can only be spent in specific categories.

Or it cannot be transferred to specific individuals.

This is not theoretical. It has been tested in pilots.

What this means:

Today your cash is yours. Spend it how you want, give it to anyone, whenever you want.

With a CBDC — the money is technically yours. But the government writes the rules.

The US Digital Dollar Political Drama:

The Digital Dollar became a politically explosive topic in America. Republicans strongly opposed it — calling it a “government surveillance tool.”

The Trump administration effectively blocked retail CBDC development through an executive order in 2025.

America’s bet is on stablecoins — a digital extension of the dollar through private companies. Not government-issued.

This is an interesting choice:

The dollar’s digital future in private hands — Tether, Circle — not the government’s. That means more freedom, less control. But it’s also a risk — private companies fail more easily than governments.

And amid all these digital revolutions — one more thing is happening that directly shapes the dollar’s future. And that thing is just one word.

Chapter 7: AI and the Dollar — What Nobody Is Saying

There’s one thing this article would have missed at its own cost.

Artificial Intelligence.

And its connection to the dollar’s future is direct.

Think about it:

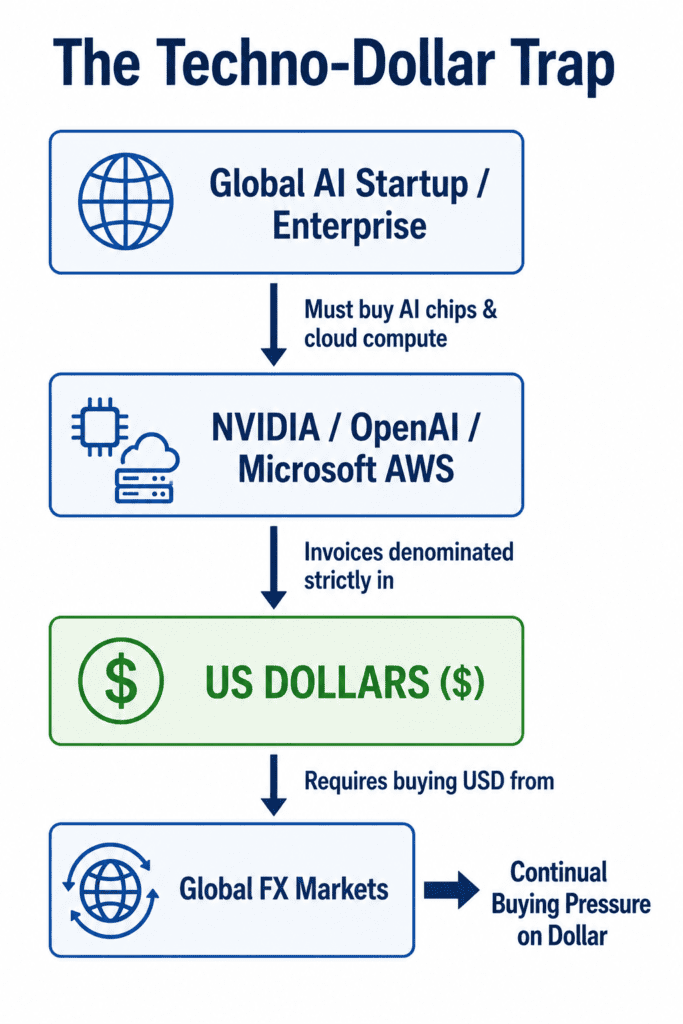

The AI revolution is happening in America right now. OpenAI. Google DeepMind. Anthropic. Meta AI. NVIDIA’s chips. All American companies or American-listed.

Global AI demand means — global dollar demand.

[FLOWCHART — “The Techno-Dollar Trap”]

NVIDIA chips in dollars. AI cloud services in dollars. AI startups globally funded in dollars. AI patents held by American companies.

Just as oil created the petrodollar in the 1970s-80s — AI could create the “techno-dollar” in the 2020s-2030s.

America’s tech dominance directly supports dollar demand. Those who say “the dollar will sink” are missing this variable.

But a warning is necessary:

Technology leadership is not permanent.

In the 1980s Japan seemed unstoppable — Sony, Toyota, semiconductor dominance. Then the bubble burst. In the 2000s Europe was the emerging market that would challenge America. Then the Greece crisis. Today America leads in AI. But DeepSeek showed in 2025 that China can build software comparable to American AI models at a fraction of the cost — which could break America’s computing monopoly.

The question isn’t whether America is leading in AI — it clearly is, right now.

The question is how long it can maintain that lead.

If China becomes a serious AI competitor — the “techno-dollar” case weakens. This is a new pillar for the dollar — but not a guaranteed one.

And there’s one more dimension people miss — AI bans and regulations.

The world is not blindly accepting American AI tools. Resistance has already begun:

Italy, March 2023 — temporarily banned ChatGPT. The first Western democracy to restrict a major AI tool. Cited privacy and data concerns.

EU AI Act, 2024 — the world’s first comprehensive AI regulation framework. Strict restrictions on high-risk AI applications. American companies directly affected.

China — American AI tools essentially blocked. OpenAI, Google AI — unavailable in China. China is developing its own domestic AI ecosystem — outside the dollar.

India, Brazil, and others — building AI governance frameworks that could limit American AI tools’ reach in the future.

The direct connection to the dollar:

If American AI tools face global restrictions — AI services won’t be bought in dollars. The techno-dollar loop would break.

Right now this is a possibility — not a reality. American AI is still globally dominant. But those who say “AI = permanent dollar strength” are ignoring this variable.

Technology leads support the dollar only as long as the world allows that technology to be used.

Now comes the moment this entire series was written for.

No one can tell you exactly. Anyone who says “definitely” is either selling something or doesn’t understand the situation.

But we can build evidence-based scenarios.

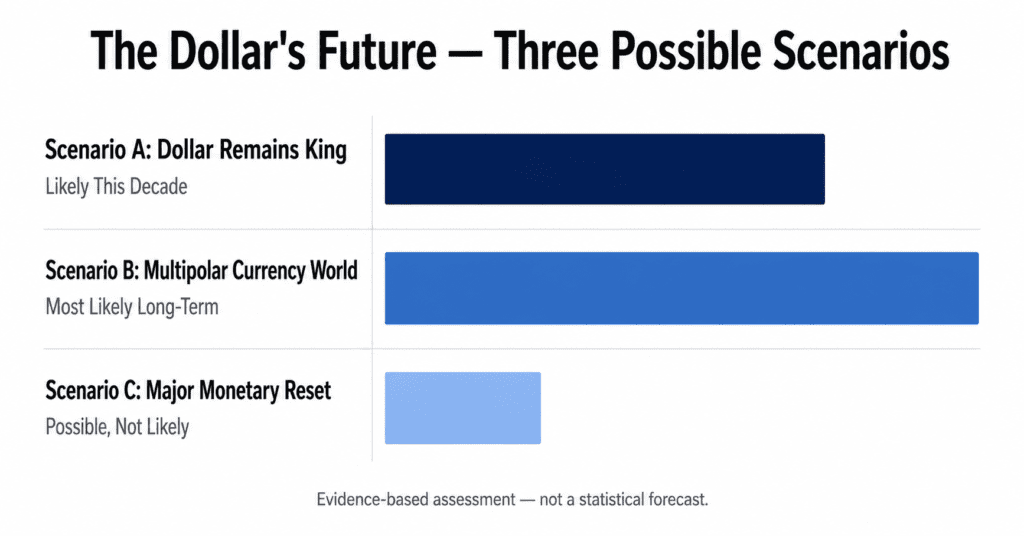

Three bars of different lengths, labels only. No specific percentages — this is a qualitative, evidence-based judgment, not a statistical forecast.

Scenario A: Dollar Remains King (Likely This Decade)

In this world, the dollar’s share stabilises at 50-55% and stops there. The yuan can’t win the race because of its capital controls. The euro’s internal politics prevent it from ever becoming #1. America stays ahead in AI — the techno-dollar loop keeps running. Stablecoins take the dollar to unexpected places — Africa, Latin America, Southeast Asia.

Debt keeps growing — but because the whole world keeps buying dollars, America keeps managing.

This is the most likely scenario this decade. The world wants change — but hasn’t found a better option yet.

Scenario B: Multipolar Currency World (Most Likely Long-Term)

In this world, no dramatic crash happens. The dollar gradually comes down to 40-45%. The yuan reaches 10-15% — if China partially opens its capital controls. The euro stays stable at 15-20%. Gold, SDRs, and regional currencies fill the rest.

No single boss — a mix will run things.

This is the 19th century model — when the British pound, French franc, and German mark all operated simultaneously in global trade. Being dominant and having a monopoly are different things.

This is the most likely long-term scenario — over the next 20-30 years. Not a crash — a slow redistribution.

Scenario C: Major Monetary Reset (Possible, Not Likely)

In this world, a major shock arrives. America’s debt becomes unsustainable. Or a major geopolitical event cracks confidence in a single blow. The world is forced to build a new system — Bretton Woods 2.0.

But here the most important question arrives — what currency does the reset land on?

If a Bretton Woods 2.0 style conference happened tomorrow, the world would find it very difficult to agree on any single new currency. China doesn’t command full trust. Europe is politically fragmented. Bitcoin is too volatile. Gold is practically limited.

This is why the most surprising possibility is — that even in a new system, the dollar doesn’t disappear entirely. Its role just shrinks. From dominant to important. From imperial to influential.

Even a reset would not be the dollar’s death. Just one more transformation.

And the pain from a forced reset would hit those who say “remove the dollar” too. India’s $700 billion+ in dollar reserves, global supply chains, oil pricing — all would be affected. This wouldn’t just be America’s problem. It would be the whole world’s problem.

Conclusion: Dollar Story — Never About Money, Always About Trust

And here we stop.

Four parts. Four decades. One thread.

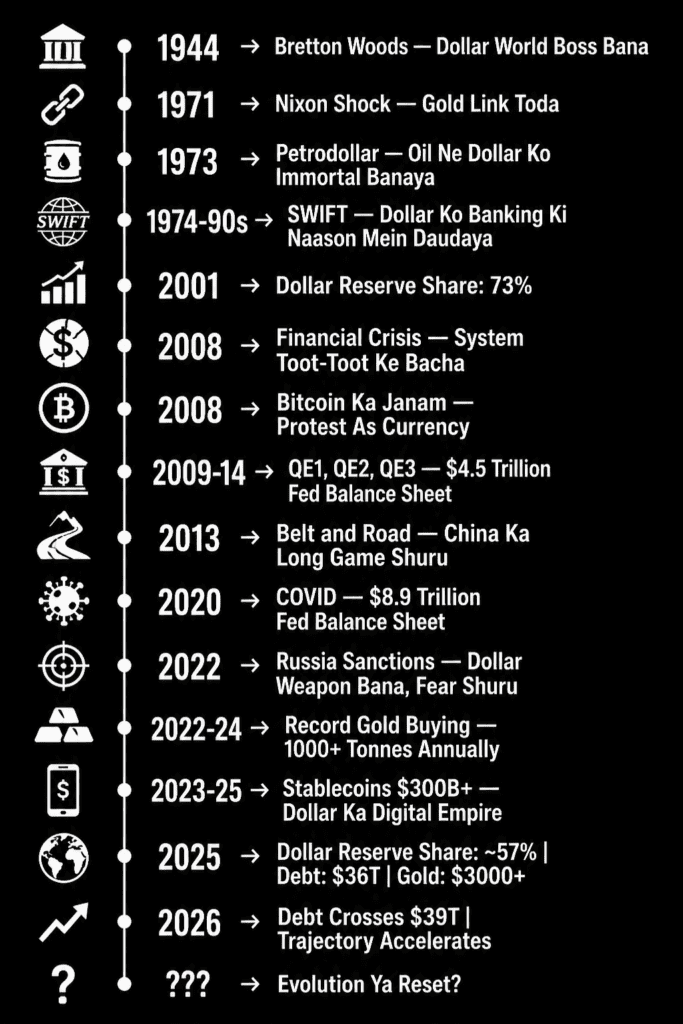

Part 1 — Birth: 1944. Bretton Woods. 44 nations. The dollar became the world’s boss — backed by a gold guarantee.

Part 2 — Rise: 1971. Nixon broke the gold link. 1973. The petrodollar was born. SWIFT ran the dollar through the veins of global banking. The dollar proved — power comes from trust, not gold.

Part 3 — Cracks: 2008. The system barely survived. QE. Bitcoin. China. Russia sanctions. De-dollarisation’s rebellion — from theory to practice.

Part 4 — Future: $39 trillion in debt (June 2026). Gold’s return. Stablecoins taking the dollar to unexpected places. CBDCs changing the definition of money. AI making a new case for the dollar. And three possible futures.

The Dollar Story was never about money.

It was always about trust.

Trust was built at Bretton Woods — with a gold guarantee.

Nixon tested it — the gold was cut, but the dollar survived. Why? Because oil sustained the trust.

2008 shook it — the system barely survived. Why did it survive? Because there was no alternative.

Russia’s freeze in 2022 turned it into a weapon — and trust started cracking. That’s why the world is taking practical steps.

And today the world is comparing the dollar against alternatives.

Perhaps the dollar’s next chapter isn’t about its death.

It’s about its evolution.

A reserve currency that was gold-backed. Then oil-backed. Then simply trust-backed. And perhaps ahead — technology-backed. Stablecoin-extended. AI-strengthened.

Everything the dollar lost — it found something new to take its place.

That has been its strength. And that will be its next test.

Dollar Story — Complete Timeline:

Bretton Woods Conference — 1944 44 nations crown the US Dollar as the world’s primary reserve asset, backed explicitly by gold at $35 an ounce.

The Nixon Shock — 1971 President Nixon unilaterally breaks the gold link. The era of pure fiat currency (trust-backed paper) begins globally.

The Petrodollar Accord — 1974 A strategic deal with Saudi Arabia ensures global oil is priced exclusively in greenbacks, creating an endless loop of global demand.

Global Financial Crisis & Bitcoin — 2008 The legacy banking system cracks, prompting the birth of quantitative easing (money printing) and the launch of decentralized crypto.

The Sanctions Weaponization — 2022 The freezing of Russia’s $300 Billion reserves scares global central banks, igniting a record-breaking physical gold rush.

The Digital & Techno-Dollar Era — 2025-2026 Stablecoins cross a $300 Billion market cap to fund US debt, while American AI leadership anchors a new wave of global currency demand.

Detailed Year-By-Year Reference:

[Dollar Story ends here. Rupee Story coming soon — India’s own economic journey, from British colonial drain to today’s $700 billion reserves.]

[Subscribe to the Ugaateyraho newsletter — so you don’t miss this story.]

FAQ

Will the dollar collapse by 2025 or 2030?

No. The dollar still accounts for ~57% of global forex reserves, 80%+ of global trade financing, and the majority of SWIFT transactions. No credible alternative is ready — the yuan due to capital controls, the euro due to political fragmentation, Bitcoin due to volatility. The dollar will transform — it won’t crash.

How dangerous is America’s $39 trillion debt?

Serious, not immediately catastrophic. It was $36 trillion in late 2025 — by early 2026 it had already crossed $39 trillion. Japan’s debt-to-GDP is ~260% and it’s still functional. But America’s debt is globally held. FY2025 interest payments were $952 billion — exceeding defence for the first time. Moody’s stripped the AAA rating. The trajectory is concerning — especially if global dollar confidence cracks.

Will stablecoins replace the dollar?

The opposite will happen. USDT and USDC are ~80% backed by US Treasuries. The $300 billion stablecoin market has made issuers significant buyers of US government debt. Bitcoin set out to bring the dollar down — stablecoins enlisted in the dollar’s army.

What is a CBDC and why could it be dangerous?

Central Bank Digital Currency — issued directly by a central bank. Legal tender like physical cash, but entirely digital. No intermediary bank — straight into your wallet. The real risk: programmable money — the government could theoretically set an expiry date on your wallet funds, or freeze them. China’s e-CNY pilots have tested these features. America blocked retail CBDC development in 2025 — betting on private stablecoins instead.

Why is gold returning?

Nixon broke the gold link in 1971. Russia’s freeze in 2022 delivered a lesson — dollar reserves can be frozen, physical gold cannot. 1,000+ tonnes of central bank buying annually in 2022-2024. Gold won’t become a reserve currency again — but as a neutral insurance asset, it has permanently returned. Nixon removed gold from the system — the system called it back 50 years later.

What is AI’s connection to the dollar?

The AI revolution is running through American companies — OpenAI, Google, Anthropic, NVIDIA. Global AI demand = global dollar demand. AI chips in dollars, AI services in dollars, AI startups funded in dollars. Just as oil created the petrodollar — AI is creating “techno-dollar” demand. But it’s not guaranteed: DeepSeek showed China can compete, and AI bans (Italy, EU AI Act) could weaken the loop if American AI faces global restrictions.

The 2008 Crisis, Money Printing, Bitcoin, and the Rebellion Against Dollar Dominance [← Read Part 2: Dollar Story Part 2 — How the Dollar Became King] Quick Answer — What’s in This Article? What was the 2008 financial crisis? A global financial meltdown triggered by the collapse of the subprime mortgage market — Bear Stearns,…

America Ka Debt, Gold Ki Wapasi, Stablecoins Ka Raaz Aur Dollar Ke Teen Possible Futures [← Part 3 padhne ke liye yahan click karein: Dollar Ki Kahani Part 3 — Jab Dollar Ka Dil Rukne Wala Tha] Quick Answer — Is Article Mein Kya Milega? Dollar marega kya? Nahi — lekin badlega zaroor. Koi bhi…

Quick Answer What is the Techno-Dollar? The idea that just as Saudi oil created sustained global dollar demand in the 1970s — American AI may be doing something similar today. The AI stack is heavily dollar-denominated at the infrastructure layer — from chips to cloud to frontier model access. As the world buys AI infrastructure,…

From the Nixon Shock to the 2025 Tariffs — Why Does India Keep Paying the Bill for Someone Else’s Emergency? Prologue: My Game, My Rules We all remember that one kid from the neighbourhood cricket match who owned both the bat and the ball. As long as he was winning, everything was fine. Standard rules….

“This article is also available in Hinglish — Dollar Ki Kahani Part 1 padhne ke liye yahan click karein” How a Broke Young Country Created the World’s Most Powerful Currency Today, the US dollar feels almost untouchable. Oil is priced in it. Global trade runs through it. Countries hold it in reserves. And whenever there’s…

Quick Answer: In June 2026, India did two things that looked contradictory. It offered to absorb hedging costs to attract foreign currency deposits — and separately, signaled an informal cap on how much foreign money it wants in its government bond market. Both moves come from the same place: foreign capital is valuable, but it’s…