This article is also available in Hinglish — Dollar Ki Kahani Part 2

To read Part-1 of The Dollar Story – Click Here

Nixon Shock, Petrodollars, SWIFT — The Story of a System That Runs the World

August 15, 1971. A Sunday night.

People across America were watching TV. Nobody was expecting anything dramatic. Sunday nights are usually quiet.

Then suddenly — the regular programme was interrupted.

President Richard Nixon appeared on screen. He looked serious. He leaned into the mic and said something that would change the global economy forever:

“I have directed Secretary Connally to suspend temporarily the convertibility of the dollar into gold.”

Just a 15-minute speech.

But the consequences? They’re still playing out more than fifty years later.

Economists around the world predicted the same thing — the dollar is finished. A currency with no gold behind it simply cannot survive.

They were completely wrong.

This was actually the beginning of the dollar’s dominance.

Quick Recap: How Did We Get Here?

In Part 1, we saw —

1944. Bretton Woods, New Hampshire. 44 countries sat together. World War II was almost over. A new global financial order was needed.

The decision: The dollar would be the world’s reserve currency. Every dollar would be backed by gold at $35 per ounce. Every other currency would be pegged to the dollar.

America held roughly two-thirds to three-quarters of the world’s gold at the time — exact figures vary by source, but the dominance was clear. The deal made sense.

But this system had a time bomb built into it.

And in 1971, it went off.

Chapter 1: Cracks in the System

The 1960s. America is deep in the Vietnam War.

Wars are expensive. Very expensive. On top of that, President Lyndon Johnson is running his ambitious “Great Society” welfare programmes. Both at the same time.

Spending is going up. Revenue isn’t keeping up.

So what did America do? It started printing dollars.

The problem — under Bretton Woods, every new dollar needed gold sitting in the vault behind it. But gold was limited. Dollars were not.

The rest of the world noticed.

France’s President Charles de Gaulle said it publicly — “America is printing dollars and getting a free lunch from the world.”

He wasn’t wrong.

France acted on it. In 1965, de Gaulle started converting France’s dollar reserves into gold and repatriating that gold back from America. Some popular accounts say France literally sent a ship to New York to collect the gold — that’s the dramatic version. What’s confirmed is that France aggressively converted its dollar holdings into gold and brought it home.

America handed over the gold. Because that was the deal.

Then other countries joined the queue.

By 1971, America’s gold was draining fast. In August, France came back — asking for more gold. Switzerland had already stepped out of Bretton Woods.

Nixon called his 15 top advisors to Camp David. Three days. Secret meetings. Nobody was allowed to make outside calls. Federal Reserve Chairman Arthur Burns was there. Treasury Secretary John Connally was there. Future Fed Chairman Paul Volcker was there too.

The decision: Close the gold window.

And on the night of August 15, 1971 — Nixon told the world.

Chapter 2: Nixon Shock — Why Didn’t the Dollar Crash?

“Temporarily” — that’s the word Nixon used in his speech.

The gold window was closing “temporarily.”

Economists were horrified. The dollar will collapse. Countries will reject it. America’s financial power is over.

But here’s what actually happened:

The dollar dipped — briefly. It fell about 7.5% against the German Deutschmark over a few months.

Then it stabilised.

Then it got stronger than before.

Why?

Because the dollar’s power was never really about gold. It was about one thing — trust and dependency.

The entire global financial system was already running on dollars. Contracts were in dollars. Trade was in dollars. Central bank reserves were in dollars. That doesn’t change in a day.

But could the dollar survive permanently without any backing? It needed a new anchor.

That anchor was found — in a desert.

To read full official history of Nixon Shock – Click Here

Chapter 3: Oil, the Desert, and the Real Petrodollar Story

October 1973.

The Yom Kippur War. Israel vs Arab nations. America backed Israel.

The Arab oil-producing countries — OPEC members — were furious. They cut off oil exports to America — the Oil Embargo.

The result? Oil prices went from $3 to $12 per barrel in just three months — a jump of over 300%. Long queues formed at petrol stations across America. Rationing began.

But this crisis also created an opportunity.

Saudi Arabia suddenly had a flood of petrodollars — enormous amounts of dollars coming in from oil sales. What were they going to do with all of it?

This is where Henry Kissinger — America’s Secretary of State — made his move.

June 1974. The US-Saudi Joint Commission on Economic Cooperation.

Officially — an economic cooperation agreement. America would provide Saudi Arabia with technical and military aid. Saudi Arabia would invest its oil revenues into US Treasury bonds.

This arrangement was revealed to the public in 2016 through a Bloomberg FOIA request.

A quick myth-bust here:

Many people say — “There was a secret treaty where Saudi Arabia agreed to sell oil only in dollars.”

No such explicit clause existed.

What actually happened: pricing oil in dollars was already the dominant practice in international markets before 1974 — no single deal created it. Saudi Arabia even continued accepting British pounds for some time after 1974. The real deal was about petrodollar recycling — Saudi oil money flowing into US Treasuries in exchange for military protection.

By 1975, all OPEC nations had adopted dollar pricing for oil — one by one.

The petrodollar system wasn’t the result of one signed agreement. It was an arrangement that evolved strategically, diplomatically, and economically.

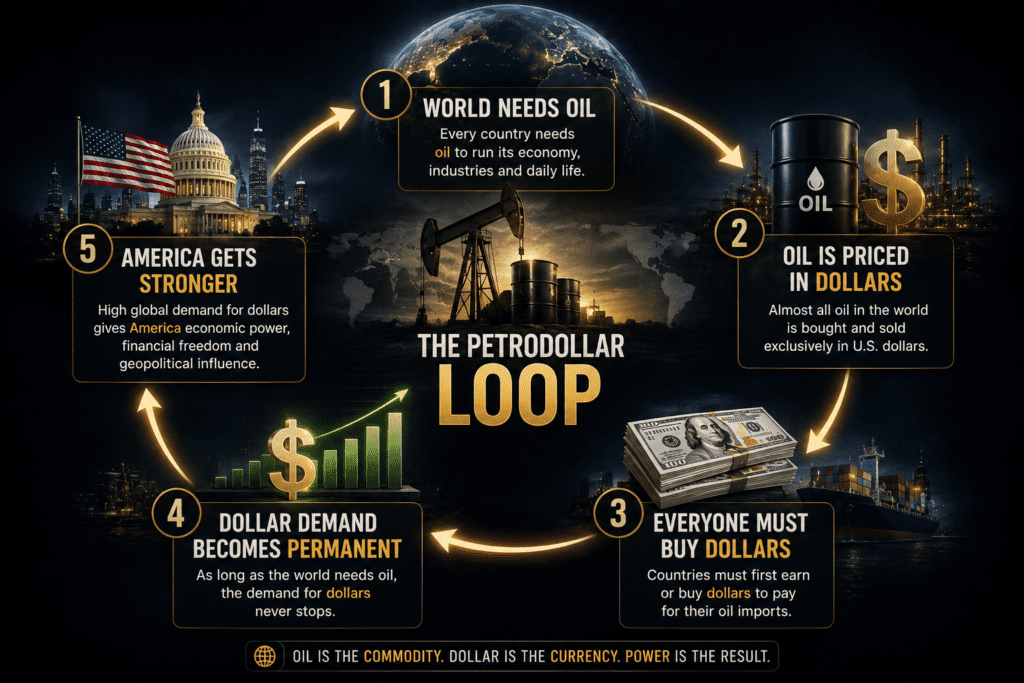

Chapter 4: The Petrodollar Loop

The dollar’s biggest strength was never gold.

It was this loop:

Think about it — Japan needs oil. Germany needs it. India needs it. Saudi Arabia won’t take yen or rupees. Bring dollars first.

So every country had to keep dollars in reserve — just to buy oil.

Without gold, the dollar had found a new anchor in oil.

Today, the majority of global oil trade — roughly 70–80% — is dollar-denominated. Exact figures vary by source, but dollar dominance in large-value cross-border oil transactions is clear.

The dollar had stopped being just a currency. It had become infrastructure — like the electricity grid. Nobody thinks about it day to day, but without it, everything stops.

Chapter 5: The Marshall Plan — How the Dollar Got Into Europe

Let’s go back to 1948.

World War II is over. Europe is completely devastated. Germany is in ruins. France, the UK, Italy — all badly damaged economies.

America stepped in with the Marshall Plan. $13 billion (worth well over $150 billion in today’s terms) — for European reconstruction.

Generous, yes. But nothing in economics is purely generous.

The aid came in the form of dollars. Europe mostly used those dollars to buy American machinery and goods. Dollar reserves settled permanently into European central banks. The dollar became deeply embedded in Europe’s financial system.

The Soviet Union understood this game. They rejected the Marshall Plan — and pressured their allied countries to do the same. They knew it was the first step toward dollar dependency.

They weren’t wrong.

The Marshall Plan rebuilt Europe. And it permanently planted the dollar in the European financial system.

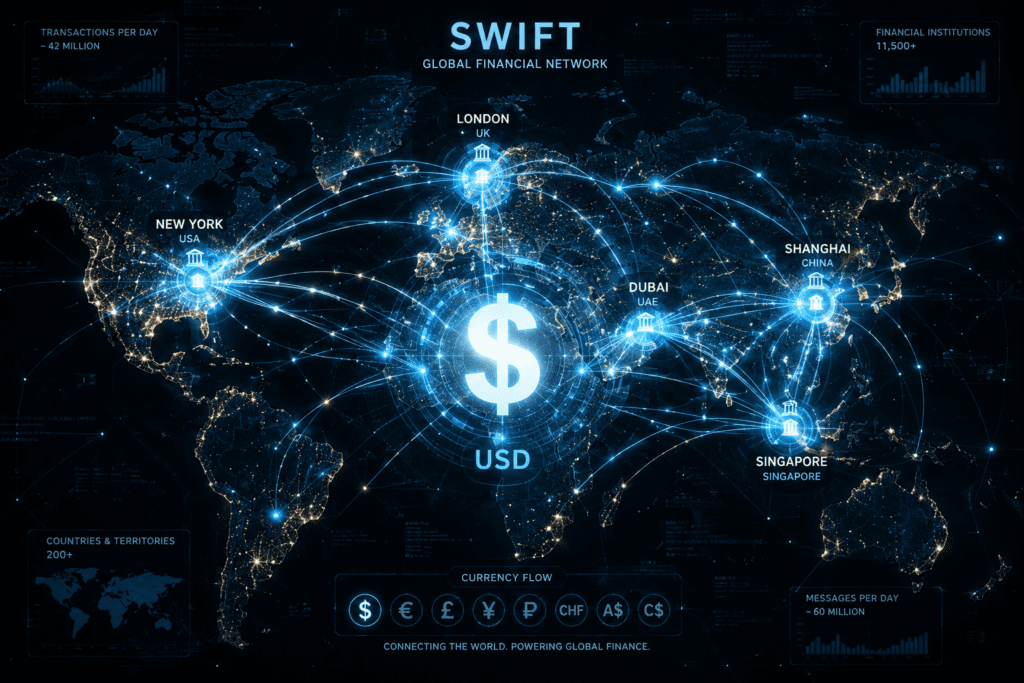

Chapter 6: SWIFT — The Dollar’s Digital Backbone

1973. Belgium.

239 banks, 15 countries. A new system was created — SWIFT (Society for Worldwide Interbank Financial Telecommunication).

Before this, banks communicated through telex machines — slow, error-prone, insecure. SWIFT replaced all of that with a fast, standardised, secure messaging system.

Today — 11,000+ financial institutions across 200+ countries are connected through SWIFT.

SWIFT is technically currency-neutral — transactions can happen in any currency. But because the dollar is the dominant trade currency, industry estimates suggest the overwhelming majority of large-value cross-border payments are dollar-denominated.

And here’s where the geopolitics gets interesting.

2012: Iran was partially removed from SWIFT — over its nuclear programme. Iran couldn’t sell its oil because the payment route was cut off. The economy took a serious hit.

2014: When Russia annexed Crimea, removal from SWIFT was threatened. Russia said at the time — “That would be equivalent to declaring war.”

February 2022: Russia invaded Ukraine. The Western response — Russia’s 10 largest banks were removed from SWIFT.

France’s Finance Minister called it a “Financial Nuclear Weapon.”

He was right. Overnight, Russia’s ability to receive international payments was severely damaged.

That’s the dollar’s digital power.

Chapter 7: The Lock-In — Why Is It So Hard to Leave?

If the dollar is such a weapon, why don’t countries just build an alternative together?

The dollar’s biggest strength isn’t gold or oil.

It’s network effects.

Think about WhatsApp.

Maybe Signal is technically better. But you use WhatsApp because your family, friends, clients and colleagues are all there. If you move to Signal alone, you’re talking to yourself.

The dollar works exactly the same way:

- More trade happens in dollars → more countries hold dollars

- More countries hold dollars → more reserves are in dollars

- More reserves in dollars → more financial instruments in dollars

- More financial instruments → even more trade in dollars

This loop is so deep that no single country can break it alone.

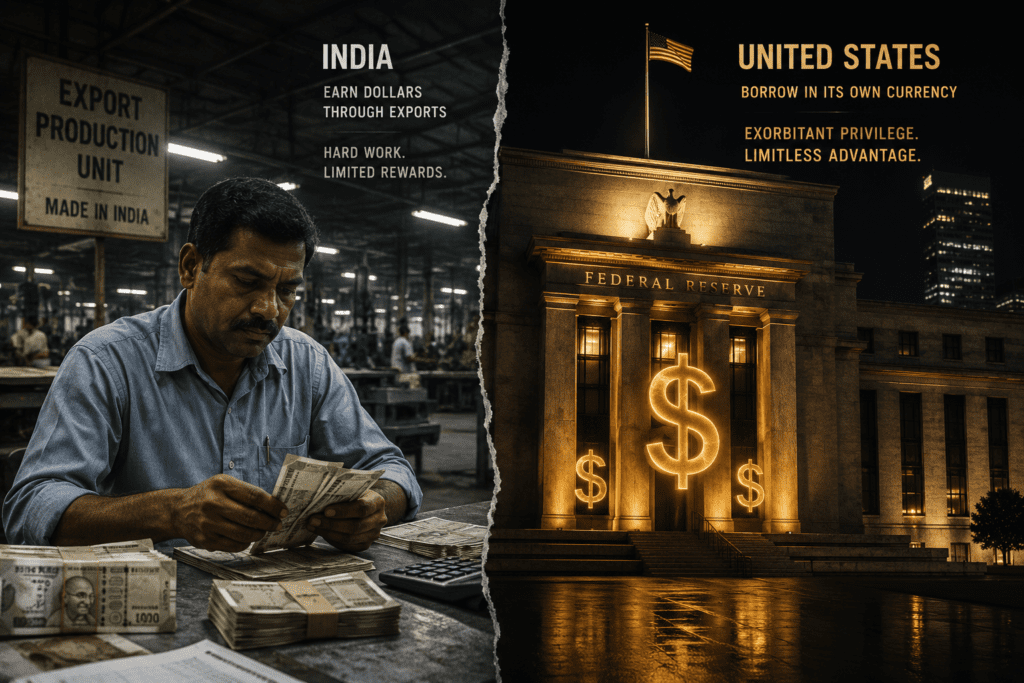

Chapter 8: Exorbitant Privilege — The Dollar’s Superpower Moment

Say India wants to buy oil.

India has rupees. But Saudi Arabia typically won’t accept rupees for international oil trade — the bill comes in dollars. So India has to earn dollars first — through exports, IT services, remittances. Earn first, then buy.

That’s the reality for most countries.

Now let’s talk about America.

America has run a trade deficit — importing more than it exports — for decades. And yet, America never stops buying.

Because America borrows in its own currency. The world needs dollars, so the world buys US Treasury bonds — effectively lending money to the American government.

If India tried printing unlimited rupees, the rupee would crash. Inflation would spiral. The IMF would show up with a bailout. That doesn’t happen to America. Because the demand for dollars is structural — built into the global system.

French economist Valéry Giscard d’Estaing gave this a name in the 1960s: “Exorbitant Privilege.“

He was complaining. But he was telling the truth.

This isn’t just an economic advantage — it’s the foundation of American superpower status. If the dollar lost its reserve currency position, America would have to do what India does. Earn first, then buy.

America knows this. That’s why protecting dollar supremacy isn’t just economic policy for America — it’s a national security issue.

Chapter 9: The Challengers — Is the King’s Throne at Risk?

So will the dollar stay dominant forever?

Nothing lasts forever in history. The British pound was the world’s reserve currency for around 200 years. Then the World Wars destroyed Britain’s economic base. The dollar replaced it.

So who’s next in line?

The Euro?

Strong currency. Stable. But the European Union is politically fragmented — Greece’s debt crisis, Italy’s borrowing problems, Germany vs Southern Europe. There’s no unified “Euro Treasury” the way the US Treasury works. The euro hasn’t seriously challenged the dollar.

The Yuan / Renminbi?

China is pushing hard — yuan-denominated trade with BRICS nations, Russia-China oil deals in yuan. But there’s a fundamental problem: capital controls. China doesn’t allow its currency to flow freely. A reserve currency needs trust and openness. China isn’t fully there yet.

Interesting idea. But for now — too volatile, no state backing. Not a realistic reserve currency candidate today.

But change is happening.

According to IMF COFER data (Q4 2025) — the dollar’s share of global reserves was 73% in 2001. Today it’s around 56.9% — the lowest since 1995.

The dollar is still king. But the court is slowly shifting.

Conclusion: A Piece of Paper — This Much Power?

In 1971, the world thought the dollar was dead.

More than fifty years later, it’s still standing at the centre of global finance.

The gold backing went away. But oil took its place. After oil came SWIFT. After SWIFT came network effects. And slowly, the dollar stopped being just a currency — it became infrastructure.

The question isn’t why the dollar is powerful.

The question is — if this system ever changes, what comes next?

The yuan? The euro? Some digital currency? Or something that doesn’t even exist yet?

And if the dollar falls — what does that mean for the rupee in your pocket? What happens to India’s economy?

That’s the story of Part 3.

[Part 3 coming soon — subscribe to the Ugaateyraho newsletter so you don’t miss it]

FAQ

Q: What exactly happened during the Nixon Shock of 1971?

On August 15, 1971, President Nixon announced that the dollar would no longer be convertible into gold — meaning no government or central bank could exchange their dollars for American gold anymore. This effectively ended the Bretton Woods system.

Q: What is the petrodollar system and how does it work?

The petrodollar system is an informal arrangement where global oil trade is primarily conducted in US dollars. If Japan wants to buy oil from Saudi Arabia, Japan first has to buy dollars, then buy the oil. This creates a constant, structural demand for dollars. By 1975, all OPEC nations were pricing oil in dollars. Today, roughly 70–80% of global oil trade remains dollar-denominated.

Q: Was there really a secret US-Saudi petrodollar deal?

Not quite. Dollar-denominated oil pricing was already the dominant practice before 1974 — it wasn’t created by any single deal. In June 1974, a US-Saudi Joint Commission on Economic Cooperation was formed, where Saudi Arabia agreed to invest its petrodollar surpluses into US Treasury bonds in exchange for military assistance. This arrangement was revealed publicly in 2016 through a Bloomberg FOIA request. There was no explicit “sell oil only in dollars” clause. The petrodollar system evolved — it wasn’t signed into existence.

Q: What is SWIFT and what does it have to do with the dollar?

SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a messaging system connecting 11,000+ financial institutions across 200+ countries for international transactions. It was created in Belgium in 1973. SWIFT is technically currency-neutral, but because the dollar dominates global trade, industry estimates suggest the overwhelming majority of large-value cross-border payments go through in dollars. Being cut off from SWIFT effectively disconnects a country from the global financial system — as Russia found out in 2022.

Q: What is “Exorbitant Privilege”?

A term coined by French economist Valéry Giscard d’Estaing in the 1960s. It refers to the unique advantage America has because the dollar is the world’s reserve currency — America can borrow in its own currency, and the world funds it by buying US Treasuries. Every other country has to earn foreign currency before it can spend internationally. America doesn’t. This isn’t just an economic edge — it’s the foundation of American superpower status.

Q: Can the yuan replace the dollar?

Not anytime soon. The dollar’s share of global reserves has declined from 73% in 2001 to around 56.9% (IMF COFER, Q4 2025) — the lowest since 1995. But the yuan has a core problem: China maintains capital controls and doesn’t allow its currency to be freely convertible. A reserve currency requires openness and trust. China isn’t there yet. No serious challenger to the dollar exists right now — though history suggests no dominance lasts forever.