The 2008 Crisis, Money Printing, Bitcoin, and the Rebellion Against Dollar Dominance

[← Read Part 2: Dollar Story Part 2 — How the Dollar Became King]

Quick Answer — What’s in This Article?

What was the 2008 financial crisis? A global financial meltdown triggered by the collapse of the subprime mortgage market — Bear Stearns, Lehman Brothers, and AIG fell in sequence. The US government rescued the system with a $700 billion TARP bailout.

What is Quantitative Easing? The Federal Reserve‘s tool of creating new digital dollars to buy bonds — injecting cash into the banking system. From 2008 to 2022, the Fed’s balance sheet expanded from $900 billion to $8.9 trillion.

Why was Bitcoin created? On 31 October 2008 — weeks after Lehman Brothers collapsed — the anonymous Satoshi Nakamoto published the Bitcoin whitepaper. The idea: a fixed-supply currency outside the control of banks and governments.

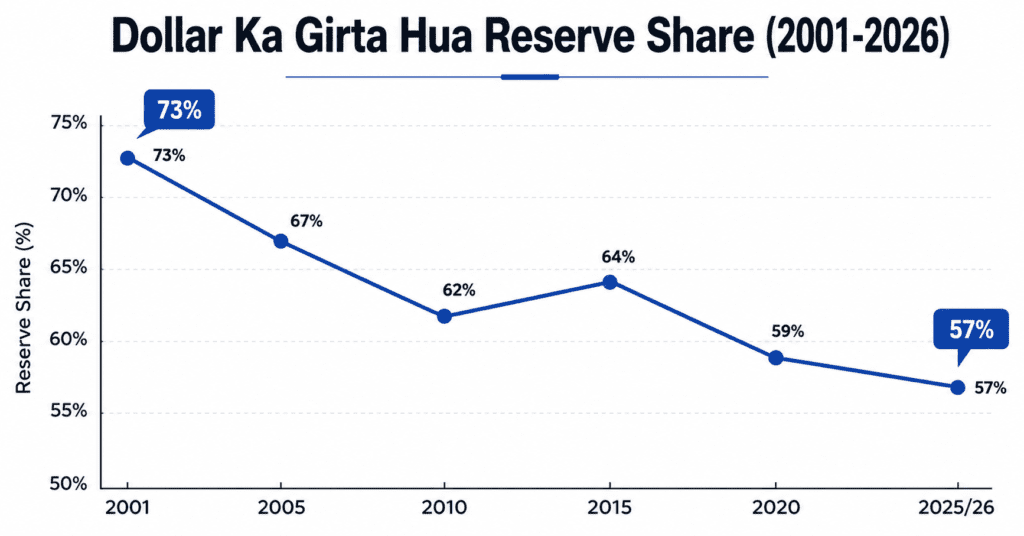

What is de-dollarisation? The dollar’s share of global reserves falling from 73% in 2001 to ~57% in 2025/2026. A real decline — but “the dollar is finished” remains a wild exaggeration.

First, a Quick Recap

In Part 1, we saw the dollar’s birth. That room at Bretton Woods where 44 nations chose the dollar as the world’s ultimate boss.

In Part 2, we saw the dollar’s muscle. Nixon cut the gold link. Kissinger engineered the petrodollar. SWIFT wired the dollar into the veins of global banking. Network effects finished off the competition.

The result? The dollar stopped being just a currency — it became the world’s economic operating system.

Now, Part 3.

This is the story of when a virus entered that operating system so dangerous, it nearly stopped its heart forever.

Prologue: When Does a King Truly Fear?

A king doesn’t fear when enemies attack from outside. A king fears when the walls of his own palace begin to crumble from within.

That’s exactly what happened in 2008.

The dollar’s enemy wasn’t another country. The dollar’s enemy was America itself. Its own greed. Its own Wall Street giants. Their over-confidence.

And if the dollar had sunk that day — it wouldn’t just have been America going down. Iceland would have gone down. Europe would have gone down. Asia would have gone down. India would have gone down.

Because the dollar had become such an enormous web that if it shook, the entire world would have been caught in it.

Let’s walk into that Wall Street party — where everyone was completely, dangerously drunk.

Chapter 1: The Party Where Everyone Lost Their Minds

2000s America. One word — BOOM.

The economy was shooting up like a rocket. Stock markets were touching the sky. And real estate? Real estate had its own special swagger.

Owning a home is the most powerful symbol of the American Dream. And in the 2000s, banks made that dream so cheap — almost recklessly cheap.

Banks were screaming: “Take a loan! Take a loan!” Politicians were saying: “Everyone deserves to own their home!” TV experts were declaring: “Property prices can never fall — that would defy gravity!”

So what happened?

A part-time waiter? Here’s your home loan. A taxi driver with irregular income? You too. A teacher with zero savings? Just sign here, the house is yours.

Ability to repay? Optional. Loans were going to everyone.

These risky loans were given a posh-sounding name: Subprime Mortgages.

What is a Subprime Mortgage? A home loan given to borrowers with poor credit history or unstable income. “Sub” + “prime” — below prime quality borrower. Higher default risk, higher interest rate. In 2000s America, these were handed out without proper verification.

But the party was raging and everyone was happy. Banks assumed property prices would keep rising forever.

Then someone realized — someone had spiked the punch bowl.

Chapter 2: Wall Street’s Most Diabolical Scheme

Now comes the most diabolical part of this story. Banks had given out the loans — but they knew the borrowers were low quality. So they pulled off a masterstroke.

They packed thousands of these risky loans into one big bag. Stamped a shiny investment label on top. And called them: Mortgage Backed Securities (MBS) and Collateralized Debt Obligations (CDOs).

The names sound like nuclear physics. The concept was simple:

“Bundle thousands of weak home loans together. Create a new product. Sell it to investors around the world. Monthly mortgage payments will keep flowing — investors collect them. The bank takes its commission and steps aside.”

What are MBS (Mortgage Backed Securities)? An investment product created by bundling thousands of home loans. Investors receive monthly payments when borrowers pay their EMIs. When borrowers default — investors lose their money.

What is a CDO (Collateralized Debt Obligation)? A product one layer above MBS. Different quality loans and bonds mixed together. The risk was so complex that even the rating agencies couldn’t understand it — yet they gave it AAA ratings.

Europe’s biggest banks bought them. Asian pension funds bought them. Insurance companies bought them.

Everyone thought — “Brilliant! The risk has been spread!”

But there was a fundamental flaw. The risk had only been spread — it hadn’t disappeared.

Think of it this way: Extract venom from a poisonous snake and distribute it into 50 small vials — hand each vial to a different investor. The poison has spread, it’s gone into different hands — but its potency hasn’t diminished. The day those vials are opened, the venom will do its work everywhere.

MBS and CDOs were those vials. Toxic debt was inside.

And in 2007-2008, people stopped paying their mortgages. The vials began to open.

Chapter 3: The Domino Effect — They Fell One by One

This crisis didn’t arrive in a single night. It was a slow-motion trainwreck — everyone could see it coming, but no one could hit the brakes.

[Bear Stearns] → [Fannie & Freddie] → [Lehman Brothers] → [AIG] → [TARP]

March 2008 — First Domino: Bear Stearns

A major Wall Street investment bank, so poisoned by subprime exposure that it collapsed. To prevent panic, the US Government gave JP Morgan Chase a $30 billion government guarantee and essentially said — “Buy this sinking ship.”

Taxpayer money entered the rescue operation for the first time. But the market didn’t hear this warning.

First week of September 2008 — Second Domino: Fannie Mae & Freddie Mac

America’s two largest mortgage giants — between them they held or guaranteed roughly $5 trillion in mortgages. When subprime losses surfaced, both teetered on the edge of collapse.

The US Government took control overnight — effectively nationalizing them. Two private companies — government-owned by morning.

This was the moment everyone knew. This crisis is not small.

15 September 2008 — Third Domino: Lehman Brothers

Pick up the newspaper that morning and the headline reads:

“LEHMAN BROTHERS FILES FOR BANKRUPTCY”

Lehman Brothers. 158 years old. Founded in 1850. Survived two World Wars. Survived the Great Depression. One of Wall Street’s biggest names.

Gone overnight. Reduced to ash.

This time the government didn’t save it. Bear Stearns had been saved. Fannie-Freddie had been saved. Lehman was let go.

Whether that decision was right or wrong — economists still debate it today. The consequence? Devastating.

16 September 2008 — Fourth Domino: AIG

The moment Lehman fell — insurance giant AIG came to the edge of collapse. AIG had issued credit guarantees on subprime mortgages. When those mortgages turned toxic — the guarantees came back to haunt AIG.

This time the government intervened — an $85 billion emergency loan. Because AIG was so deeply connected to so many players that letting it fall would have been worse than Lehman.

October 2008 — Fifth Domino: TARP

A $700 billion proposal arrived before Congress — the Troubled Asset Relief Program (TARP). To buy toxic assets from banks.

Congress rejected it in the first week. Markets crashed further. Then after debate — it was approved.

The American public was furious: “The banks made the mistake — so why is our tax money bailing them out?”

The question was legitimate. But the alternative was Great Depression 2.0. So everyone held their breath.

Chapter 4: When the World Held Its Breath

The moment Lehman fell — the entire financial system froze for a beat.

Why? Because no bank trusted any other bank anymore. Everyone was thinking — the institution across from me might be holding a vial of poison.

Think about it — if a pandemic broke out in your neighbourhood and you had no idea how many houses were infected, would you open your door to anyone? No.

Credit froze. Money stopped moving. Banks stopped lending. Companies couldn’t make payroll. The system jammed.

In financial markets, a credit freeze is the equivalent of blood stopping in the human body — instant death.

2008-2009 — The Numbers: IMF, World Bank, and Federal Reserve Data:

| What Happened | Scale of Damage |

|---|---|

| Global equity markets | $10 trillion+ in value wiped out |

| American household net worth | Fell by $13 trillion |

| US unemployment | ~10% by 2009 |

| Iceland | Entire banking system wiped out overnight |

And this wasn’t just America’s problem.

Iceland’s entire banking system was wiped out overnight. European pension funds were devastated. India felt it too — software companies and exports took a significant hit.

The dollar’s global reach — its greatest strength — had now become a curse for the entire world.

One country’s mistake. The whole world’s pain.

Chapter 5: When the Doctor Gave the Patient “New Blood”

Federal Reserve Chairman Ben Bernanke and Treasury Secretary Hank Paulson had exactly two options:

Either let the entire system drown — Great Depression 2.0.

Or do something that had never been done before in history.

They chose the second path.

December 2008: The Fed cut interest rates to 0–0.25% — effectively zero. The first time in US history rates had gone this low. Borrowing money became essentially free for banks.

But when even that didn’t work — the Federal Reserve pulled out its most powerful weapon.

Name: Quantitative Easing — QE.

What is Quantitative Easing (QE)? A monetary policy tool in which a central bank (like the Federal Reserve) creates new digital dollars and uses them to buy government bonds and financial assets from the market. The goal — inject cash into the banking system so banks start lending again and the economy moves. Technically different from traditional “money printing” — assets are exchanged — but the net result is a significant expansion of the money supply.

In plain language: imagine the banking system is a patient whose blood has been poisoned. The doctor (the Federal Reserve) sits at a computer, creates new digital dollars, and uses that money to buy the bad bonds and toxic assets sitting on banks’ books. Fresh cash flows into the banks. They start lending again. The economy’s heart begins beating again.

Critics screamed: “This is cheating! Fake money printing!”

Supporters said: “This is economic CPR — without it the patient would have died!”

Both were right in their own way.

Chapter 6: One Trillion… Two Trillion… Three Trillion…

The scale of QE was enough to blow a normal person’s fuses.

America ran not one, not two — but three rounds:

- QE1 (November 2008 – March 2010): ~$1.75 trillion — bought MBS and Treasury bonds

- QE2 (November 2010 – June 2011): ~$600 billion in Treasury bonds

- QE3 (September 2012 – October 2014): Open-ended — buying assets every month for as long as needed

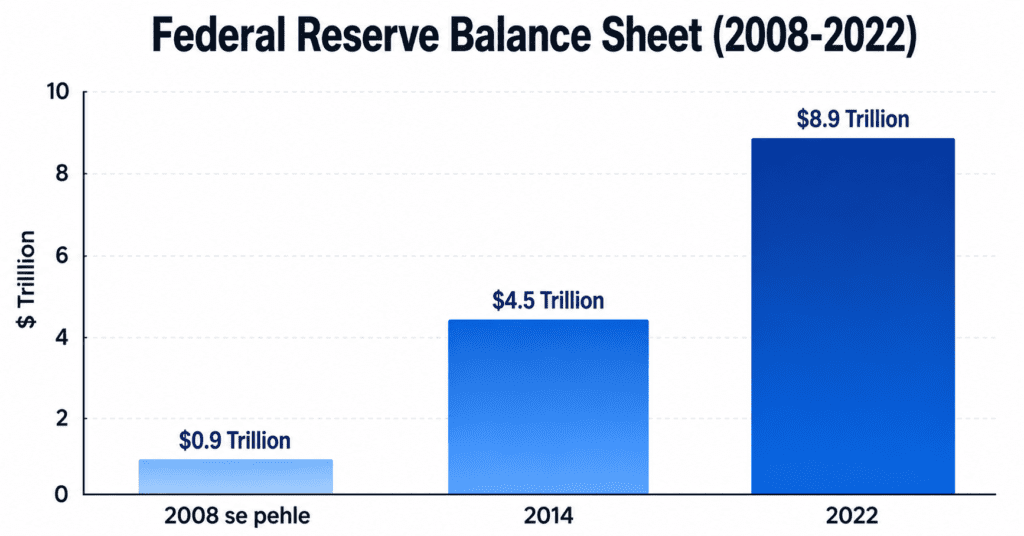

Federal Reserve Balance Sheet — The Real Tally of QE:

| Year | Balance Sheet Size | What Happened |

|---|---|---|

| Before 2008 | ~$900 Billion | Normal size |

| 2014 (Post QE1+QE2+QE3) | ~$4.5 Trillion | 5x expansion |

| 2022 (Post COVID QE) | ~$8.9 Trillion | Roughly 10x expansion |

In just 14 years — roughly 10 times larger.

And it wasn’t just America. The European Central Bank, Bank of Japan, Bank of England — all ran their own versions of QE.

Thoughtful people around the world began asking one question:

“If the dollar runs purely on trust — can America print unlimited money? Does this have an expiry date or not?”

And in the middle of that anger and that question — in a dark corner of the internet, an anonymous individual was building something. Something that could challenge the entire world of fiat currency.

Chapter 7: That Mysterious Halloween Message of 2008

31 October 2008.

Wall Street was in chaos. On that exact same day — a small cryptography mailing list received a silently dropped 9-page PDF.

The sender’s name: Satoshi Nakamoto.

Who is Satoshi? No one knows to this day. One person? A group? Indian? Japanese? American? The mystery is still alive.

The paper’s title: “Bitcoin: A Peer-to-Peer Electronic Cash System”

Satoshi’s simple argument: “Why should we trust these banks and governments? They reduce the value of our money whenever they want. They print unlimited amounts. They bail out their friends. We will build a currency that no one can control.”

What is Bitcoin? A decentralized digital currency — no central bank, no government control. Supply is permanently fixed: only 21 million Bitcoin will ever exist. Transactions are recorded on a blockchain — a public, tamper-proof ledger. Created as a direct response to the 2008 crisis.

3 January 2009 — Bitcoin’s first block was mined — known as the Genesis Block. Embedded in the block data was a headline from the UK’s The Times newspaper:

“Chancellor on brink of second bailout for banks”

This was no ordinary timestamp. This was a direct slap across the face of the entire fiat currency system.

Bitcoin was born as a protest.

22 May 2010 — Bitcoin Pizza Day

Florida developer Laszlo Hanyecz gave away 10,000 Bitcoin. In return he received — 2 Papa John’s pizzas.

This was Bitcoin’s first real-world commercial transaction. At the time the world laughed — “What a madman!”

The value of those 10,000 Bitcoin today? Billions of dollars.

Laszlo’s regret? Perhaps. His place in history? Permanent.

By 2011, Satoshi gradually disappeared from the internet — leaving the project in the community’s hands. To this day no one knows who he was.

Today Bitcoin’s market cap is in the trillions. Reserve currency? Still a very long way off — one tweet moves the price 20% in either direction, and no serious economy can run on such a roller-coaster. But the idea Satoshi introduced — that money shouldn’t be state-controlled, that supply should be fixed — that thinking has continued to influence the world. And will keep doing so.

Chapter 8: China’s Quiet Chess Move

While America was licking its wounds from 2008 — another player was very quietly setting its pieces on the board.

China.

China joined the WTO in 2001. After that? Factories in China. Supply chains in China. “Made in China” — everywhere in the world.

2010: China overtook Japan. Became the world’s second-largest economy.

The question was now direct: “If we do all the manufacturing, if the whole world buys from us — why is the reserve currency the dollar? Why not our Yuan?”

China began working systematically:

China’s De-dollarisation Strategy — Timeline:

| Year | Move |

|---|---|

| 2009 | Yuan internationalisation program launched |

| 2013 | Belt and Road Initiative — 60+ countries |

| 2015 | CIPS (Yuan payment system) launched |

| 2016 | Yuan included in IMF SDR basket |

| 2023-24 | Yuan oil pricing discussions with Saudi Arabia |

2013: Belt and Road Initiative — roads, ports, railways, pipelines across 60+ countries. Chinese investment. And naturally — transactions in yuan.

2023-2024: The Wall Street Journal and Reuters reported serious discussions between Saudi Arabia and China about pricing oil in yuan. But those conversations have remained conversations — in 2023, Saudi Arabia reaffirmed dollar pricing for most of its oil trade. A new tunnel has been dug into the dollar’s fortress — but the fortress still stands.

China’s old problem, however, remains — Capital Controls.

In China, an ordinary citizen can only take $50,000 in foreign exchange out of the country per year. Companies need strict government approval too. The yuan is not freely convertible.

Simple logic: if a bank told you — “Deposit your money here, but you need our permission to take it out” — would you put your life savings there? Absolutely not.

A reserve currency requires openness and trust. China is not willing to give up its control.

But China is patient. And the direction is clear.

Chapter 9: 2020 — Same Drama, This Time on Steroids

March 2020. COVID-19.

The world froze. Literally. Airlines grounded. Factories shut. Restaurants closed. People locked inside their homes.

Stock markets fell as though someone had pushed them from behind. The crash speed markets recorded in the first two weeks — not even the Great Depression had seen that.

And central banks pulled out the same old remedy — but this time in double dose.

America’s COVID Fiscal Response — Breakdown:

| Package | Amount |

|---|---|

| CARES Act (2020) | $2.2 Trillion |

| American Rescue Plan (2021) | $1.9 Trillion |

| Other packages | ~$0.9 Trillion |

| Total | ~$5 Trillion |

Separately, the Federal Reserve’s balance sheet — already at $4.2 trillion — reached $8.9 trillion in just two years. Money was being created like confetti at a wedding.

In the short term, the system was saved.

In the long term, what every first economics textbook warns about happened:

More money + Fewer goods = Prices up.

June 2022 — US inflation hit 9.1%. The highest in 40 years. Europe felt it too. India felt it — petrol, cooking oil, lentils — everything more expensive.

The cost of unlimited printing — it arrives late. But it always arrives.

March 2023 — One More Reminder: Silicon Valley Bank

Just when everyone thought things were back on track — Silicon Valley Bank (SVB) collapsed. The favourite lender of the tech and startup world. In a single day.

Why? SVB had bought large quantities of long-term government bonds during COVID — when rates were low. When the Fed raised rates to fight inflation — the value of those bonds fell. Depositors panicked and began withdrawing money. Classic bank run.

The second-largest bank failure in US history at that point — and weeks later, First Republic Bank collapsed too, even larger than SVB.

This was a reminder — the system rebuilt after 2008 still has cracks. When the QE hangover wears off, side effects appear.

Chapter 10: 2022 — The Year That Changed the Rules

February 2022. Russia invaded Ukraine.

America and Western nations, in anger, took two significant steps:

- Kicked Russia out of SWIFT

- FROZE Russia’s $300 billion+ in foreign exchange reserves overnight

That one move shook central banks around the entire world.

India, China, Saudi Arabia, Brazil — all of them realized one thing:

“Russia had $300 billion in dollar reserves — America zeroed it out in one move. Tomorrow, if we have a falling-out with America — our money could be frozen too.”

The dollar was no longer just a currency — it had become a geopolitical weapon.

And from that fear, the real rebellion was born:

India’s move: Began buying discounted crude oil from Russia — not in dollars, but in Rupees and UAE Dirhams. For the first time, India created a bilateral trade mechanism to bypass the dollar.

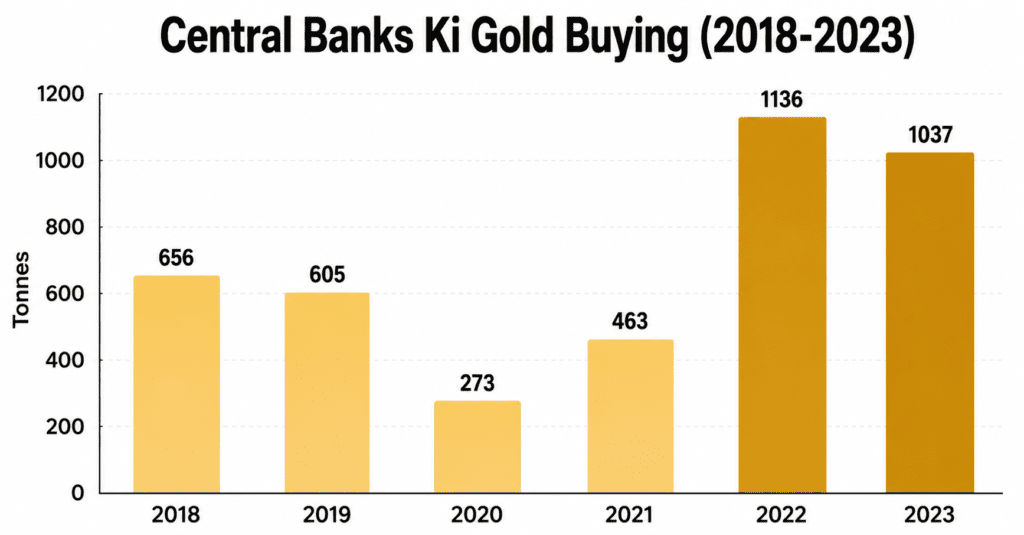

The gold tsunami:

Central banks began buying gold at record-breaking levels:

- 2022: 1,136 tonnes — highest since the 1950s

- 2023: 1,037 tonnes — almost equally high

- Poland, China, Turkey, and RBI — all among the top buyers

This wasn’t just investment. This was a signal — searching for alternatives to dollar reserves.

De-dollarisation was no longer just academic discussion. Practical steps had begun.

Chapter 11: De-dollarisation — Real or Hype?

Social media is full of videos every day — “Dollar finished! BRICS currency coming! Dollar has turned to dust!”

And on the other side: “Nothing will happen. Dollar will always be king.”

Both are wrong.

What is De-dollarisation? The process by which countries gradually reduce their use of the US dollar in trade, reserves, and financial transactions. This is not the dollar’s “end” — just a gradual decline in dominance.

The Dollar Is Still King — The Data:

| Metric | Dollar’s Share |

|---|---|

| Global forex reserves (IMF COFER Q4 2025) | ~56-57% |

| Global trade financing | ~80%+ |

| SWIFT transactions | Majority |

| Global debt issuance | Dominant |

But the decline is real:

2001: 73% Global Forex Reserve Share

↓ Slow but steady

2025/26: ~57% Global Forex Reserve Share

= 16 percentage points down in 24 yearsBRICS expanded in 2024 — Saudi Arabia, UAE, Iran, Egypt, Ethiopia joined. By PPP-based estimates, BRICS now represents roughly 35%+ of global GDP — though that figure is significantly lower on a market exchange rate basis. PPP is a valid measure, but context matters.

Alternatives to SWIFT are also being built: China built CIPS (Cross-Border Interbank Payment System). Russia built SPFS. BRICS is working on a digital payment system called “BRICS Bridge” — still in early stages, but the direction is clear.

An Honest Reality Check on the Challengers:

| Challenger | The Problem |

|---|---|

| Chinese Yuan | Capital controls — $50,000/year limit. Trust deficit. |

| Euro | Fragmented politics. No single Treasury. |

| BRICS Currency | India-China tensions. Member priorities clash. |

| Bitcoin | Extreme volatility. No serious economy runs on a roller-coaster. |

India’s Specific Picture:

India’s forex reserves in 2025 stand at ~$700 billion+ — mostly dollar-denominated. The Rupee has depreciated roughly 40%+ against the dollar from 2008 to 2025 — this is total depreciation, not per year.

If the dollar system changes — India’s imports, inflation, and external debt costs will be directly affected.

So what happens next?

The dollar won’t crash overnight. The world is moving toward a multipolar currency world — much like the 19th century when the British pound, French franc, and German mark all circulated simultaneously. Instead of one boss, a mix will run things.

The king still sits on the throne. But the court is changing.

Conclusion: The Strangest Thing About Trust

In 1971 people said — “The dollar will collapse.” It didn’t.

In 2008 it seemed — “The dollar system will break.” It survived.

In 2020 — “Unlimited printing will kill the dollar.” Still alive.

The dollar has proved every bad prediction wrong.

But some things are now clearly visible:

2008 showed — the system is fragile. Bear Stearns, Fannie-Freddie, Lehman, AIG — one after another. Saved with $700 billion of taxpayer money.

2020 showed — there is no visible limit to printing. $8.9 trillion. And consequences arrive with a delay — in the form of 9.1% inflation in 2022.

2022 showed — the dollar can be weaponised. And that realisation converted de-dollarisation from theory into practice. 1,000+ tonnes of gold annually. CIPS. Rupee-ruble trade. Yuan oil discussions.

The dollar’s real power was never gold. Never oil. Never SWIFT.

The throne still belongs to him,

But cracks have appeared in the walls.

The question is no longer about the dollar’s power —

Now it is about the world’s trust.

The dollar’s real power was — the world’s TRUST.

And the most dangerous thing about trust?

It takes years to build. Once it starts breaking — it becomes very hard to stop.

The British pound learned this lesson over 40 years — from the World Wars to Bretton Woods. The dollar is still king.

But for the first time in 50 years — the world isn’t just talking. It’s taking practical steps.

And those steps open a very large question — if the dollar’s share keeps falling, if America’s debt keeps rising, if new players like gold and stablecoins are entering the arena — what happens to the dollar over the next 10-20 years?

Will this king hold his throne? Or will the throne itself be redesigned — without the dollar disappearing?

In Part 4:

Dollar’s Future — Will the King Die, or Become More Powerful? How serious is America’s debt problem? Can the printing go on forever? Why is gold quietly returning? And stablecoins — which look like crypto’s rebellion — how are they actually making the dollar stronger? Three possible futures — and which one is most likely.

[Part 4 coming soon — subscribe to the Ugaateyraho newsletter so you don’t miss the biggest chapter yet]

FAQ — People Are Also Asking

What was the 2008 financial crisis and what was its connection to the dollar?

he 2008 crisis began with the collapse of the US subprime mortgage market. Banks gave risky loans — Subprime Mortgages — to low-quality borrowers. Wall Street bundled those loans into MBS and CDOs and sold them globally. When these products turned toxic, dominoes fell — Bear Stearns, Fannie Mae, Freddie Mac, Lehman Brothers, AIG. The government rescued the system with $700 billion through TARP. The dollar-based global system was so interconnected that the crisis reached Iceland, Europe, and Asia. For the first time, it showed seriously that a dollar-centric system could be fragile.

What is Quantitative Easing (QE)? How is it different from money printing?

In QE, the Federal Reserve creates new dollars and buys government bonds and financial assets — injecting liquidity into the system. Technically different from money printing — assets are exchanged, not one-way creation. Practically the effects are similar — money supply increases significantly. Three rounds: QE1 (~$1.75T), QE2 (~$600B), QE3 (open-ended). Fed balance sheet went from $900B to $4.5T. Then $8.9T after COVID. The 9.1% inflation of 2022 was the delayed consequence.

Why was Bitcoin created? What is its connection to the dollar?

Bitcoin was born as a direct response to the 2008 crisis. On 31 October 2008, anonymous Satoshi Nakamoto published the whitepaper — fixed supply (21 million max), no central authority. On 3 January 2009 the Genesis Block was mined — with The Times headline embedded: “Chancellor on brink of second bailout for banks.” A direct comment on the entire fiat money system. 22 May 2010 — Bitcoin Pizza Day: 10,000 BTC for 2 pizzas, Laszlo Hanyecz. That value today — billions. Bitcoin was born as a protest — reserve currency status is still a very long way off.

Why did the 2022 Russia sanctions accelerate de-dollarisation?

Russia’s $300 billion+ in dollar reserves were frozen overnight. The rest of the world thought — “Our reserves could be frozen tomorrow too.” That fear accelerated practical steps — India’s rupee-ruble trade, Saudi-China yuan oil discussions, central banks’ record gold buying (1,000+ tonnes annually in 2022-2023). De-dollarisation moved from theory to practice.

What is de-dollarisation? Is the dollar really dying?

The dollar’s share has come down from 73% in 2001 to ~57% (IMF COFER Q4 2025/early 2026) — a real decline. But “dollar finished” is still an exaggeration. The yuan isn’t ready due to capital controls. The euro is fragmented. This is a decades-long gradual process — not a sudden crash. The direction is decline, not a cliff edge.

Can BRICS replace the dollar?

Difficult in the near future. After the 2024 expansion, BRICS represents roughly 35%+ of global GDP on PPP-based estimates. Alternatives like CIPS and BRICS Bridge are developing — but SWIFT remains dominant. India-China tensions and competing priorities among member countries — a common BRICS currency is still at the discussion stage.

What impact does the dollar system have on India?

India’s forex reserves are ~$700 billion+ — mostly dollar-denominated. The Rupee has depreciated roughly 40%+ against the dollar from 2008-2025 (total, not per year). India must import oil, electronics, machinery — all in dollars. If the dollar system changes — India’s imports, inflation, and external debt costs will be directly affected.