Quick Answer

India measures inflation in two very different ways — WPI (Wholesale Price Index) tracks prices at the factory gate, while CPI (Consumer Price Index) tracks prices in your shopping basket.

In normal times, both move together. But every few years, they dramatically diverge — factories face runaway inflation while consumers barely notice. This split is caused by energy shocks, supply chain crises, or global commodity surges. The gap cannot last forever. Eventually, someone pays — either corporate profits take the hit, or consumer prices catch up.

Understanding why this gap opens, and how it closes, tells you more about India’s economy than any single headline number ever will.

Two People. One Country. Completely Different Economies.

Somewhere in India, Raj is reading a newspaper that says inflation is under 4%.

Somewhere else, Suresh is staring at a fuel bill that says inflation is closer to 10%.

Both men are looking at the same economy.

Both think they understand what’s happening.

And both are right.

Meet Raj.

Raj opens the newspaper.

Inflation is 4%.

His grocery bill feels manageable. Petrol stings a little. The chai outside his office costs the same as last month.

Life, broadly, goes on.

Now meet Suresh.

Suresh owns a mid-sized manufacturing unit in Pune. He makes packaging materials. Nothing glamorous. Just the boxes that hold the things Raj buys.

Suresh opens his electricity bill.

Then his fuel bill.

Then his chemicals bill.

Then his transport invoice.

Then, briefly, his blood pressure prescription.

His inflation is not 4%.

His inflation is closer to 10%.

He stares at Raj’s newspaper headline.

He wonders if they are living in the same country.

Strangely enough, they are.

And both of them are correct.

How Can Inflation Be Two Different Numbers?

Because inflation is not one thing.

It depends entirely on where you’re standing in the economy.

Inflation: A sustained increase in the general price level of goods and services over time, reducing the purchasing power of money.

Think of the economy as a relay race.

A farmer grows wheat.

A factory turns wheat into flour.

A truck ships flour to a bakery.

A bakery sells bread to Raj.

Inflation can hit any leg of this race. It can hit the farmer’s fertiliser costs, the factory’s electricity bill, the truck driver’s diesel, or the bakery’s rent.

Each runner feels the pain differently.

That’s why economists use multiple measuring sticks.

CPI: The Inflation Raj Feels

Consumer Price Index (CPI): A measure of the average change in prices paid by households for a representative basket of goods and services, including food, housing, education, healthcare, and transport.

CPI is the inflation that shows up in your own life — your bag of groceries, your rent, your fuel tank.

It tracks:

- The rice you buy

- The school fees you pay

- The rent your landlord charges

- The petrol you pump

- The hospital bill you quietly cry over

Think of CPI as the answer to one question:

“How expensive is it to be alive this month?”

CPI is what the RBI targets when it sets interest rates. It’s what politicians nervously watch before elections. It’s what you feel in your wallet.

WPI: The Inflation Suresh Feels

Wholesale Price Index (WPI): A measure of price changes at the wholesale level — before goods reach consumers — covering raw materials, fuel, agricultural commodities, and manufactured goods at the factory gate.

WPI lives upstream.

It measures prices before any product reaches a shop shelf or a household. It’s the world of bulk transactions, industrial inputs, commodity markets, and factory gates.

It tracks:

- Crude oil and mineral fuels

- Steel, aluminium, chemicals

- Agricultural raw materials

- Manufactured goods in bulk

Think of WPI as the answer to a completely different question:

“How expensive is it to make things this month?”

WPI doesn’t care about your grocery bag. It cares about the cost of producing everything that eventually goes into your grocery bag.

The Normal Relationship Between WPI and CPI

In stable economic times, WPI and CPI are like two friends who walk at different speeds but generally end up at the same destination.

WPI often leads CPI by a few months. When raw material costs rise, factory gate prices rise first. Companies then gradually pass those costs on to consumers. CPI follows, usually with a lag of two to four months.

A gap of 1–2 percentage points is unremarkable. Three points raises an eyebrow. Four or five points starts conversations.

Six points?

Six points is an alarm.

That’s the moment when Raj and Suresh genuinely stop living in the same economy.

Is A 6-Point Gap Normal? No. Here’s What It Actually Means.

Let’s be specific for a moment.

In most years, WPI and CPI differ by roughly 1–2 percentage points. That’s background noise. Economists shrug.

A gap above 4 points is uncommon enough to attract attention. It usually signals something structural — not just a bad month for vegetables.

A gap approaching 6 points? That’s a diagnostic reading, not a headline number. It tells you the economy is absorbing a major external shock. The kind that has historically appeared only during:

- Global commodity supercycles (when raw material prices surge worldwide)

- Energy crises (oil shocks, supply disruptions, geopolitical conflicts)

- Post-pandemic supply chain collapses

Here’s what three episodes look like side by side:

| Period | WPI Peak | CPI Peak | Who Suffered More |

|---|---|---|---|

| Early 2010s | ~7% | ~10% | Consumers (food crisis) |

| 2022 (Post-Covid) | ~15.88% | ~7.8% | Producers (supply chain + energy) |

| 2026 (Energy shock) | ~9.68% | ~3.93% | Producers (oil prices) |

Notice the pattern.

When CPI runs above WPI, consumers are hurting and factories are relatively fine. The problem is demand-side — things are expensive to buy.

When WPI runs above CPI, producers are hurting and consumers are temporarily shielded. The problem is supply-side — things are expensive to make.

These are not the same diagnosis. They don’t have the same treatment.

India in the early 2010s had a consumer inflation problem. The RBI raised rates to cool household spending.

India in 2022 and again in more recent years has had a producer inflation problem. Raising rates helps eventually, but the root cause is external — a global energy shock that India cannot directly control.

This distinction matters enormously.

A government or central bank that treats a producer inflation problem like a consumer inflation problem — by aggressively suppressing demand — risks slowing growth without fixing the underlying cause.

The doctor needs to read both thermometers. Not just the one patients complain about.

When The Gap Opens: A Brief History of Inflation Divorces

India has experienced this inflation split before. Each episode had a different villain. Each eventually resolved the same way.

Episode One: The Food Crisis Years (Early 2010s)

In this chapter, the script was reversed.

Consumers suffered. Factories were relatively fine.

Food prices surged. Onions became a political emergency. Vegetables made headlines. Household budgets were decimated.

CPI ran comfortably above WPI for several years.

Raj was angry. Suresh was mostly okay.

The RBI raised interest rates aggressively. The government sweated. Inflation eventually cooled — though the political damage from onion prices arguably lasted longer than the inflation itself.

Resolution: Demand suppression through rate hikes, combined with better agricultural seasons.

Episode Two: The Great Supply Chain Catastrophe (2022)

Then came the event that rewrote every economics textbook written after 2010.

Covid shut down ports. Ships disappeared. Containers vanished. Semiconductor factories went dark. Every supply chain on Earth simultaneously jammed.

Then Russia invaded Ukraine. Energy prices exploded. Food commodity prices surged. Oil markets lost their minds entirely.

In India, WPI peaked at approximately 15.88% in May 2022. CPI peaked around 7.8% in the same period — painful, but significantly lower.

Factories were in genuine distress. Suresh’s 2022 diary would not make pleasant reading.

Consumers felt pain too — but a more filtered, delayed version of it.

The gap between WPI and CPI stretched to nearly 8 percentage points.

Resolution: Global commodity prices eventually cooled. Supply chains untangled. The RBI raised rates. The gap narrowed over 18 months.

Episode Three: The Energy Shock Pattern (Any Given Decade)

Here’s what both episodes have in common:

They were triggered by an external shock that hit energy prices first.

Food crisis? Oil was involved. Fertiliser prices. Transport costs.

Covid supply chain? Shipping fuel. Factory energy. Logistics.

This is not a coincidence.

India imports roughly 85% of its crude oil requirements. That single dependency means every major global energy disruption eventually becomes India’s domestic inflation problem — whether India had anything to do with the original shock or not.

Globalization’s finest feature: you can receive the bill for an event you didn’t attend.

When oil moves, it moves everything. Transport. Manufacturing. Packaging. Chemicals. Fertilisers. Logistics. Power generation.

WPI feels it immediately, because it measures the upstream world — the world of industrial inputs and energy costs.

CPI feels it later, partially, filtered through corporate decisions about what to pass on and what to absorb.

The Great Inflation Sponge

This is the most important concept in the entire article.

If factories are experiencing 10% inflation, why aren’t consumers experiencing 10% inflation?

Because someone is absorbing the shock.

Between Suresh’s factory and Raj’s shopping basket, the economy acts like a giant sponge. Inflation enters one side. The sponge tries to stop it saturating the other side.

The sponge consists of:

Corporate profit margins. Companies reduce their profits rather than raise prices. They absorb the cost difference themselves. This works until margins get too thin.

Existing inventory buffers. Companies sell from stock purchased at older, lower prices. This delays the inflation impact on consumers. It works until the old stock runs out.

Productivity improvements. Factories find ways to produce more efficiently, offsetting some cost rises. This works until the efficiency gains are exhausted.

Competitive pressure. In competitive markets, no single company wants to be the first to raise prices and lose customers. Everyone waits. Everyone absorbs. Until someone blinks.

The sponge absorbs. The sponge absorbs. The sponge absorbs.

And then the sponge gets full.

And it starts dripping.

Onto Raj’s shopping basket.

The only real question during any WPI-CPI divergence is not whether the gap will close. It always does.

The question is how it closes.

The Three Ways This Always Ends

History has only three resolutions. Every episode of WPI-CPI divergence ends in one of these — or a combination of all three.

Ending One: Companies Take The Hit

Corporations absorb the cost inflation through margin compression. Profits fall. Shareholders suffer. But consumer prices stay stable.

This is the preferred outcome for everyone except shareholders and CFOs having to explain quarterly results.

It can only last so long. Margins have floors. Below a certain profitability level, companies either raise prices or shut down.

Ending Two: Consumers Take The Hit

Companies eventually pass costs through. Consumer prices rise to catch up with producer prices. The CPI climbs toward the WPI.

This is the most common historical resolution. It’s painful for households but restores corporate health.

The RBI typically responds by raising interest rates to prevent the consumer price rise from spiralling into persistent inflation. Which means Raj gets hit twice — first by prices, then by EMIs.

Inflation rarely travels alone.

Ending Three: The Demand Collapse

Sometimes, before costs are fully passed through, demand itself weakens. Consumers start buying less. Economic activity slows. Factories reduce production. The pressure on input costs eases.

Inflation cools — but so does the economy.

This is the least comfortable resolution because it means growth suffered. But from a pure inflation-gap-closing perspective, it works.

Historical pattern: In India, Ending Two (consumer prices rising) has been the most frequent resolution, usually combined with monetary tightening by the RBI. Ending One (profit compression) plays a supporting role in the first few months. Ending Three tends to happen in global downturns, not Indian domestic cycles alone.

What The RBI Does During All This (And Why It Matters For Your EMI)

But the RBI watches WPI carefully, because WPI is a leading indicator of future CPI.

When WPI surges while CPI is still calm, the RBI faces a judgment call.

Wait and watch? Or pre-emptively raise rates?

If it waits too long, consumer inflation surprises on the upside. The RBI looks reactive. Its credibility takes a hit.

If it raises rates too early, it slows an economy that doesn’t yet have a consumer inflation problem. Growth suffers unnecessarily.

This is genuinely one of the hardest calls in monetary policy. Not because the RBI doesn’t understand the data. But because the timing of cost pass-through is inherently unpredictable. It depends on thousands of individual corporate pricing decisions made across millions of products in a $3.5 trillion economy.

What this means for Raj: even when he doesn’t feel inflation today, the WPI-CPI gap may be quietly setting up the RBI’s next interest rate decision. Which may quietly reshape his home loan EMI. Three months from now.

Economic chickens, as always, come home to roost.

India Is Also Quietly Replacing Its Inflation Thermometer

Here’s a detail that almost nobody covers.

India has been phasing in a new inflation measure: the Producer Price Index (PPI).

Producer Price Index (PPI): A measure of average price changes received by domestic producers for their output, covering all stages of production. Used by most advanced economies as an alternative to WPI.

Most developed economies — the US, the UK, Germany, Japan — use PPI rather than WPI.

The difference is meaningful. PPI is generally designed to measure price changes received by producers more directly than WPI, which is why most advanced economies prefer it.

India plans to publish WPI and PPI side by side for several years before eventually retiring WPI entirely.

In other words: even the inflation thermometer is being upgraded.

When PPI output readings have been published, they have come in remarkably close to WPI — confirming that the pressure on producers is real, not a measurement artefact.

The measurement changes. The underlying phenomenon doesn’t.

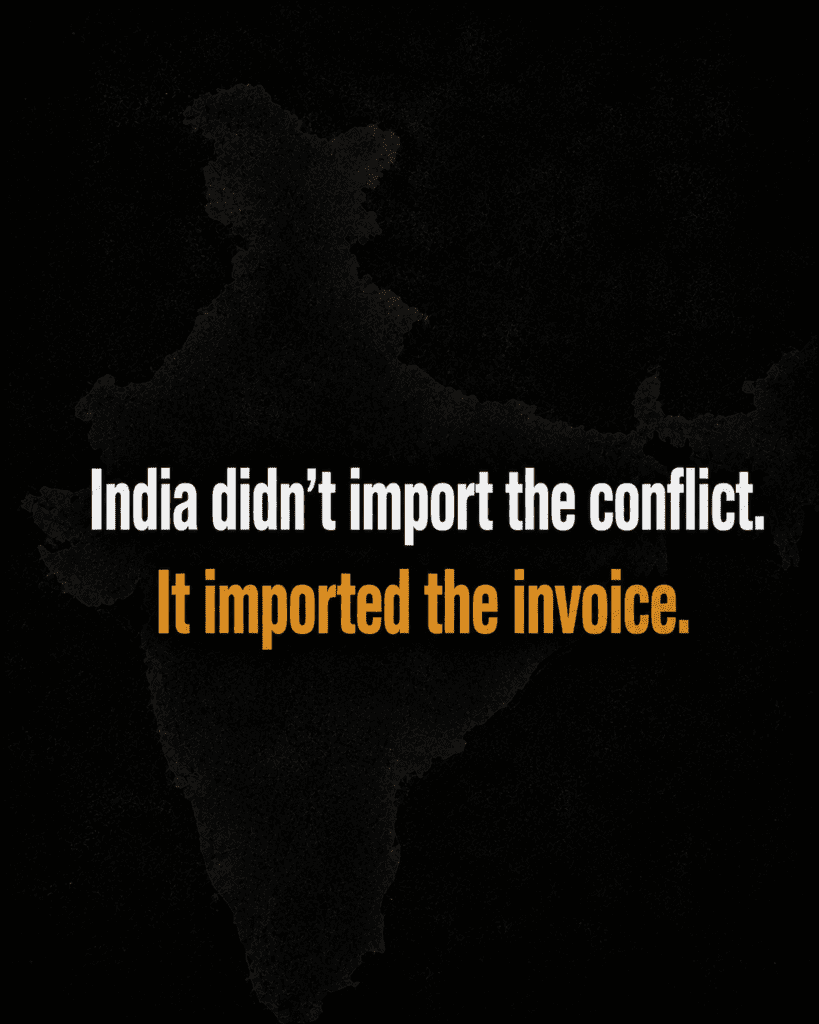

India Is Importing Inflation Again

Many people think globalisation means access to cheaper goods from around the world.

That’s the brochure version.

The fine print version reads differently: globalisation also means you import other people’s crises.

India imports roughly 85% of its crude oil requirements. That single number explains a great deal of India’s inflation history.

When oil prices rise — because of a conflict, a sanctions regime, a cartel decision, or simply a bad quarter in the Gulf — India doesn’t import the conflict.

“India doesn’t import the conflict. It imports the invoice.”

The invoice arrives at Suresh’s factory first. His energy bill goes up. His chemicals cost more. His transport bill swells. His packaging supplier raises prices.

Raj, sitting at his desk reading the newspaper, sees none of this yet.

But the invoice is already inside the economy. It’s just stuck upstream.

And it will move downstream. Always.

Suresh cannot vote in the election that started the conflict. He cannot call the oil minister of the exporting country. He has no seat at the geopolitical table where these decisions are made.

He has only his balance sheet.

And a blood pressure prescription he didn’t need two years ago.

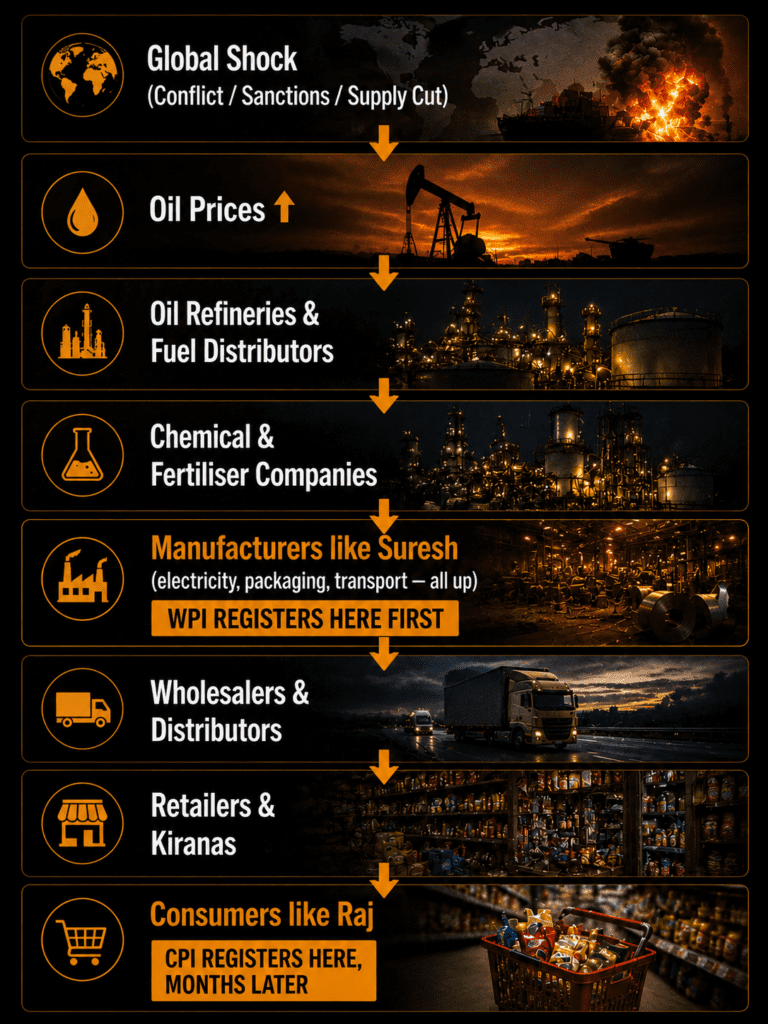

Follow The Money

Here’s the question most inflation coverage never asks.

When oil prices spike, where does the extra money actually go?

Trace the chain:

The money doesn’t disappear at any stage. It accumulates pressure — until something gives.

The money doesn’t vanish.

It flows. Upstream. Toward the source of the shock.

The WPI-CPI gap is essentially a map showing where that money is currently jammed inside the system.

A large gap means: the money has entered the economy at the producer level but hasn’t yet fully reached consumers. It’s stuck in Suresh’s margin compression, his inventory drawdowns, his reluctance to raise prices and lose customers.

A closing gap means: the money is moving. Either it’s flowing further downstream to consumers (prices rising), or it’s flowing back out through demand destruction (people buying less), or the source shock has eased and the chain is unwinding.

Inflation is never destroyed.

It is only transferred.

The WPI-CPI gap simply tells you where the bill is currently parked.

Final Thought: Who Pays?

Raj and Suresh both live in India.

They both shop in the same markets, drive on the same roads, breathe the same air.

But during the months when WPI runs far above CPI, they are experiencing genuinely different economic realities.

Suresh knows prices are brutal. He’s been absorbing costs that Raj hasn’t seen yet.

Raj knows life feels manageable. He’s benefiting from a buffer that won’t last forever.

History is clear about what happens next.

The buffer runs out.

The gap closes.

Somebody pays.

The only open question — in every episode, in every cycle, across every decade — is whether it’s Suresh’s profit margin that finally breaks, or Raj’s shopping basket that finally catches fire.

Usually, it’s a bit of both.

And the RBI is sitting somewhere in the middle, trying to make sure it’s neither too much of either.

Inflation is never destroyed.

It is only transferred.

The gap between WPI and CPI tells you where the bill is currently parked.

Today, it is parked at India’s factory gates.

Tomorrow, it may arrive in your shopping basket.

Key Takeaways

- CPI measures inflation as experienced by consumers — food, rent, education, transport, healthcare.

- WPI measures inflation as experienced by producers — fuel, raw materials, industrial inputs, factory-gate prices.

- A WPI-CPI gap of 1–2 percentage points is normal. A gap approaching 6 points signals a major supply-side shock.

- When WPI runs above CPI, India has a producer inflation problem — not a consumer inflation problem. These require different policy responses.

- India’s dependence on imported crude oil (approximately 85% of requirements) makes it structurally exposed to global energy shocks that hit WPI before CPI.

- The gap always closes — through profit compression, consumer price increases, weaker demand, or a combination of all three.

- Inflation is never destroyed. It is only transferred. The WPI-CPI gap tells you where the bill is currently parked.

- India is gradually transitioning from WPI to PPI (Producer Price Index), following global best practices.

Frequently Asked Questions

What is the difference between WPI and CPI in India?

WPI (Wholesale Price Index) measures price changes at the factory gate — raw materials, fuel, industrial inputs, and bulk manufactured goods. CPI (Consumer Price Index) measures price changes as experienced by households — food, rent, education, healthcare. WPI captures production-side inflation; CPI captures consumption-side inflation.

Why is WPI sometimes much higher than CPI in India?

When global energy or commodity prices surge, WPI rises sharply because it is dominated by fuel and raw material costs. CPI rises more slowly because corporations absorb part of the cost through margin compression rather than immediately passing it to consumers. The gap between the two reflects this absorption buffer.

Does high WPI always lead to high CPI later?

Not always. But sustained periods of high WPI often put upward pressure on CPI over time. When producers face prolonged cost increases, many eventually pass them through to consumers. However, in some episodes, corporate margins absorb much of the shock — meaning consumers never fully feel the producer-level pain. The transmission depends on competitive conditions, inventory levels, demand strength, and how long the cost pressure lasts.

What does the RBI do when WPI is high but CPI is low?

The RBI officially targets CPI, not WPI. But it monitors WPI as a leading indicator. When WPI is high and rising, the RBI may pre-emptively tighten monetary policy (raise interest rates) to prevent future CPI from overshooting its 4% target.

What is PPI and how is it different from WPI?

Producer Price Index (PPI) measures prices received by domestic producers for their output, excluding import taxes and certain distribution costs that WPI includes. PPI is considered a cleaner measure of domestic production inflation. Most advanced economies use PPI rather than WPI. India is transitioning toward PPI over the coming years.

Why does India import so much crude oil and why does it matter for inflation?

India imports roughly 85% of its crude oil requirements because domestic production is insufficient to meet demand. This makes India highly sensitive to global oil price movements. Since oil affects transport, manufacturing, chemicals, fertilisers, and power generation, any global oil price shock transmits rapidly into WPI — and eventually into CPI.

Inflation is never destroyed. It is only transferred.

The gap between WPI and CPI tells you exactly where the bill is currently parked.

This is one of the clearest explanations of WPI vs CPI I’ve read. The Raj and Suresh examples make an abstract economic concept feel real and easy to understand. The article strikes an excellent balance between educational depth and engaging storytelling. The ‘inflation sponge’ analogy is especially memorable and helps readers grasp why producer inflation and consumer inflation can diverge. Overall, a highly informative and reader-friendly piece that makes economics accessible to a broad audience.